$GEHC: An Earnings Growth Masterclass (No Paywall)

40-Page Breakdown on our Highest Conviction Pick

Our Thesis

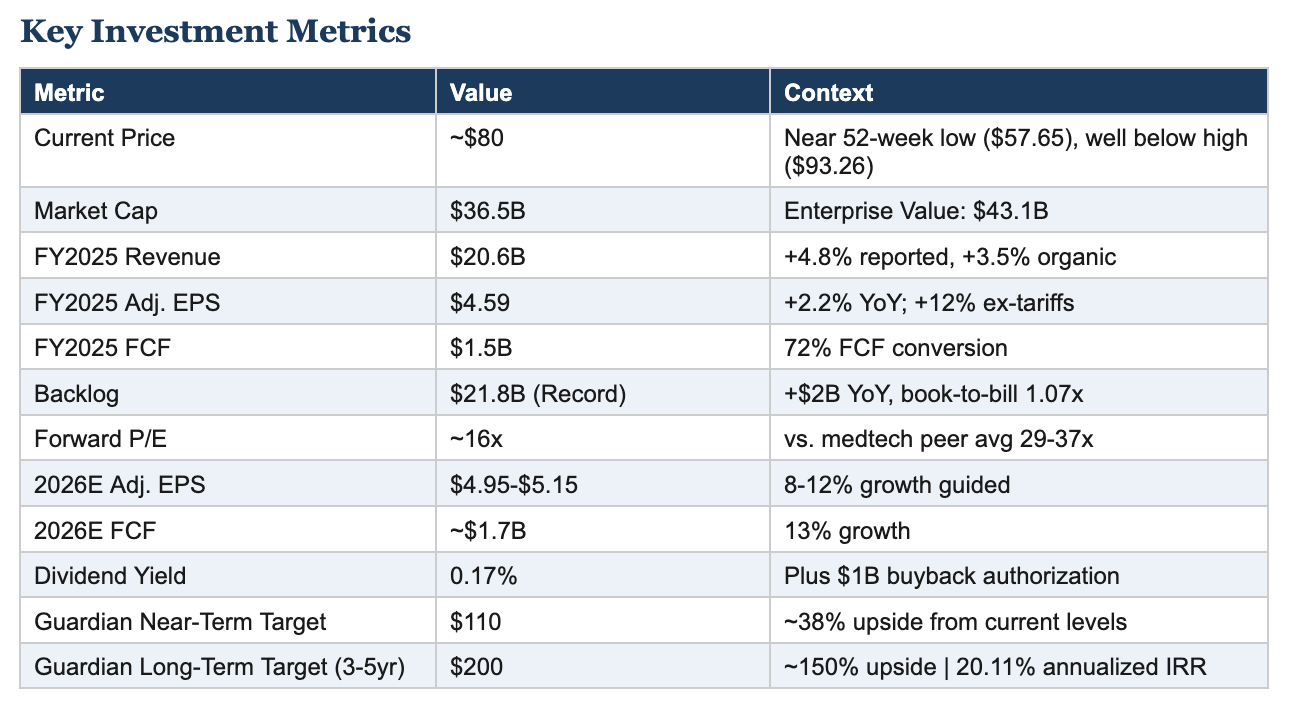

GE HealthCare Technologies (NASDAQ: GEHC) is our highest conviction idea at Guardian Research. Spun off from General Electric in January 2023, GEHC has spent three years laying the foundation for what we believe will be a multi-year earnings compounding story that the Street is only beginning to appreciate. At approximately $80 per share, the stock trades at roughly 16x forward earnings versus the medtech peer average of 29-37x. We think this discount reflects a misclassification: the market sees a cyclical equipment manufacturer weighed down by Chinese hardware competition fears. What actually exists is a $20.6 billion franchise in the early innings of a business model transformation, shifting from lumpy capital equipment sales toward sticky, high-margin recurring revenue through cloud software, AI platforms, and pharmaceutical diagnostics. That transformation is happening now, and the market is not paying for it.

We see a clear path to $110 per share in the near term as the market begins to properly value the existing earnings power, and a $200 per share long-term target over 3-5 years as compounding earnings growth and multiple re-rating deliver a 20.11% annualized IRR. The return is driven by five converging dynamics: a generational product launch cycle including Flyrcado, photon-counting CT, Freelium MRI, and AI-enabled clinical software driving top-line acceleration toward $28-30 billion by 2030; margin expansion of 300-400+ basis points from Heartbeat lean deployment, new product mix-up, tariff mitigation, and recurring revenue scaling; capital return acceleration via the $1 billion share repurchase program and growing dividend capacity; the $2.3 billion Intelerad acquisition shifting the revenue mix toward high-margin recurring SaaS; and a potential China recovery that is currently baked into guidance as a headwind, creating an embedded call option. At $200, GEHC would trade at approximately 22-24x 2030 earnings, which is still a meaningful discount to the 35x medtech peer average. Our long-term target does not require the stock to reach full fair value relative to its peer group.

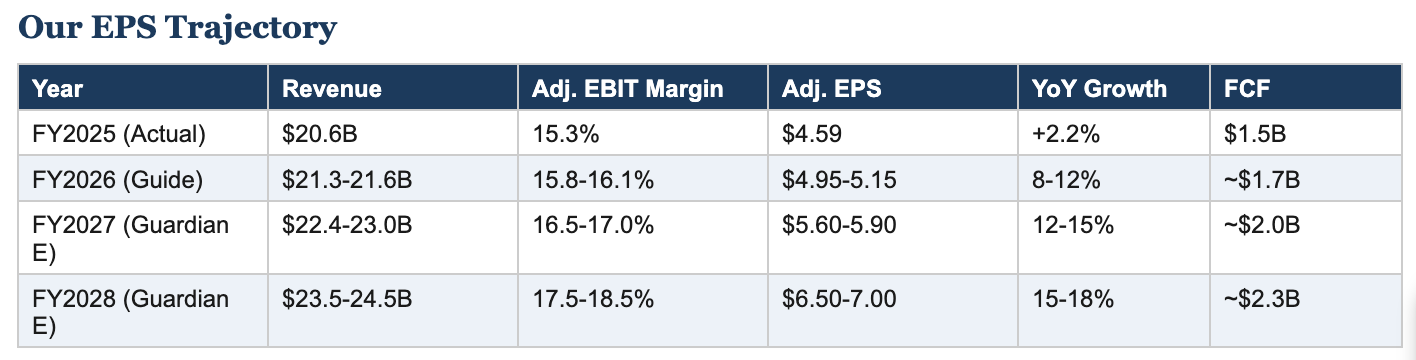

The company delivered FY2025 results that exceeded expectations: $20.6 billion in revenue (4.8% reported growth, 3.5% organic), $4.59 adjusted EPS, $1.5 billion in free cash flow, and a record $21.8 billion backlog. The number that matters most here: excluding the $245 million tariff headwind, adjusted EPS would have grown 12% and EBIT margins would have expanded. For 2026, management guided 3-4% organic revenue growth, 50-80 basis points of margin expansion, and 8-12% adjusted EPS growth to $4.95-$5.15. That guidance beat consensus estimates. We think it is conservative and that GEHC will over-deliver, as they did in FY2025.

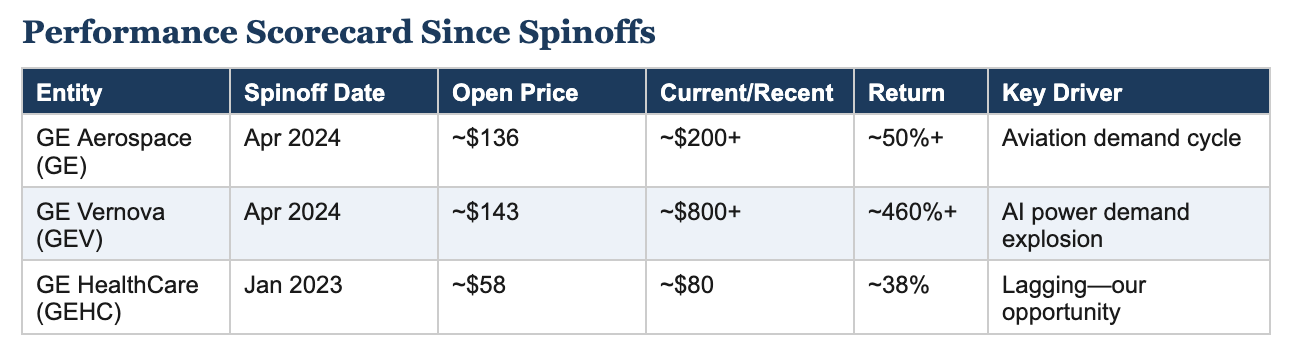

The GE spinoff playbook has already worked: GE Aerospace has more than doubled since April 2024, and GE Vernova is up 400%+ on AI-driven energy demand. GEHC, the first to separate, has lagged with only ~50% appreciation since its January 2023 IPO. We think this laggard status is temporary. GEHC is at the earliest innings of its independent value creation, and the catalysts ahead are more powerful than what has already been priced in.

THE GE TRANSFORMATION: FROM CONGLOMERATE TO THREE TITANS

The breakup of General Electric represents one of the most significant corporate transformations in American history. Under CEO Larry Culp, GE dismantled a 130-year conglomerate into three focused, world-class companies. The playbook was straightforward: unlock value by eliminating conglomerate complexity, aligning management incentives with focused operations, and allowing each business to pursue its own capital allocation and strategic priorities. The results speak for themselves.

The Three-Way Split

GE HealthCare was the first to separate, spinning off on January 4, 2023. Shareholders received 1 share of GEHC for every 3 shares of GE. The stock debuted around $58 and currently trades near $80, a roughly 50% return since inception. GE Vernova, the energy business, spun off on April 2, 2024, with shareholders receiving 1 share for every 4 shares of GE. It opened at $143 and has since surged past $800, an approximately 460% return driven by insatiable AI-powered electricity demand. GE Aerospace, the crown jewel aviation business, retained the GE ticker symbol and has more than doubled from its $136 spinoff price to over $200 as of late 2025.

The thing that jumps out: GEHC has dramatically underperformed its siblings. While GE Vernova caught the AI-energy wave and GE Aerospace rode aviation recovery, GEHC has been weighed down by China concerns and tariff headwinds. But these are transient issues. The structural advantages of independence—focused capital allocation, aligned incentives, streamlined operations, and innovation acceleration—are identical across all three entities. GEHC’s value unlock is delayed, not diminished.

Spinoff situations historically outperform the market by 10-20% in the 2-3 years following separation. GEHC is in year three of its independent existence, entering the phase where operational improvements compound into earnings acceleration. The spinoff alpha playbook is fully in motion.

MACRO THEMATIC & INDUSTRY TAILWINDS

GEHC sits at the intersection of several long-duration secular tailwinds. These are not cyclical trends; they are structural forces that will drive demand for decades. Understanding this backdrop is essential to appreciating why GEHC’s earnings growth runway extends well beyond what current consensus models capture.

Global Aging Demographics

The world is aging fast. The United Nations projects that the population aged 65 and above will double over the next 30 years, reaching 1.6 billion by 2050. In the US specifically, IBISWorld’s 2025 medical device industry report highlights that adults aged 65 and older—who account for 40% of heart disease and arthritis diagnoses—are expected to outnumber children by 2034. That is a watershed moment for healthcare demand, and it is less than a decade away. Aging populations drive exponential increases in chronic disease prevalence across cardiovascular disease, cancer, neurological disorders, and musculoskeletal conditions, all of which require diagnostic imaging for screening, diagnosis, and treatment monitoring. IBISWorld projects US medical device industry revenue to grow at a 2.2% CAGR through 2030 on the back of these demographic dynamics alone, and that is a conservative, industry-wide figure that understates the growth for premium players like GEHC who are gaining share through innovation. This is a demographic math problem, and it creates decades of volume growth for medical imaging and diagnostic platforms.

Medical Imaging Market: A $44-68B Opportunity Growing at 5%+ CAGR

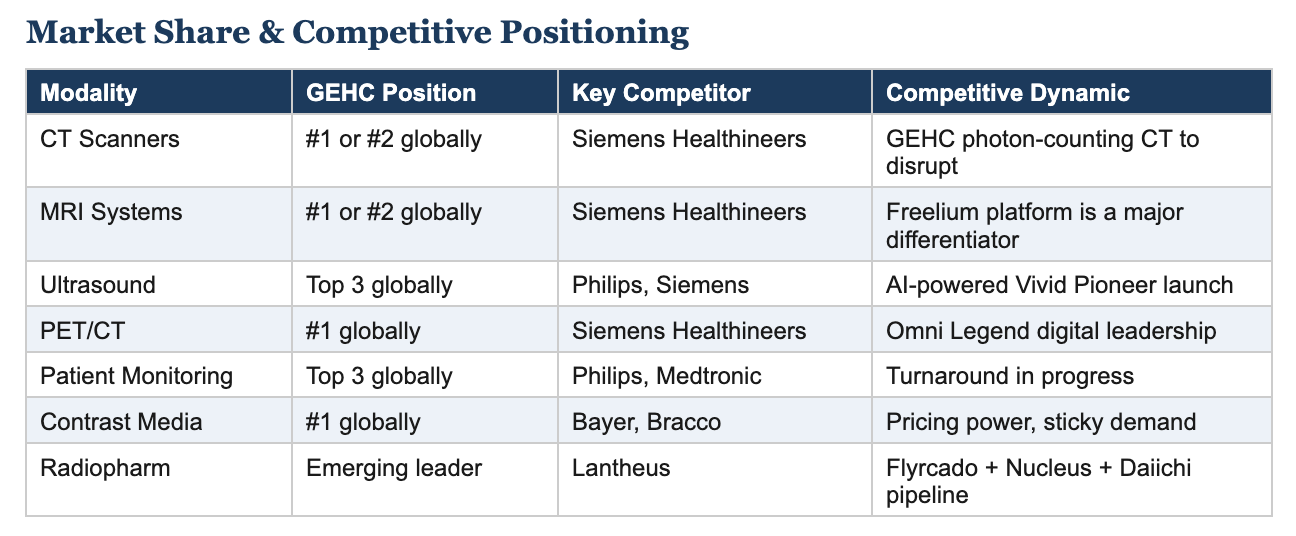

The global medical imaging market was valued at approximately $43.5-44.3 billion in 2025 and is projected to reach $64.7-68.4 billion by 2032-2033, growing at a CAGR of 5.1-6.4%. North America represents approximately 36-37% of the global market. The diagnostic imaging device segment alone was estimated at $48.9 billion in 2025, projected to reach $60 billion by 2030. Within this, MRI systems represent the largest technology segment at approximately 28% market share, followed by computed tomography, which is the fastest growing subsegment. GEHC, as the global number one or two player across nearly every imaging modality, is positioned to capture a disproportionate share of this growth.

AI-Enabled Healthcare: The Next S-Curve

Artificial intelligence is transforming diagnostic imaging from a visualization tool into a clinical decision-support engine. According to IBISWorld’s 2025 report on the US medical device industry, FDA authorizations for AI-enabled medical devices surged 31.2% as of mid-2025, a number that speaks to the explosive growth of this category. GEHC has secured more than 80 FDA-cleared AI algorithms—the most in the industry—and led the market in FDA-authorized AI devices for three consecutive years from 2022 through 2024. In October 2024, the company launched its AI Innovation Lab, a dedicated accelerator focused on developing next-generation ‘agentic AI’ solutions that autonomously assist clinicians in diagnostic workflows. This goes well beyond incremental product improvement. It is a strategic bet on AI as the next platform shift in healthcare delivery. The convergence of AI with medical imaging creates real value for GEHC in three ways: premium pricing power on AI-enhanced devices, recurring SaaS revenue from clinical software, and productivity improvements for healthcare systems facing a worsening physician and radiologist shortage. The AAMC projects a shortfall of up to 86,000 physicians across specialties by 2036, and the Neiman Health Policy Institute finds the current radiologist shortage will persist through at least 2055 without intervention. IBISWorld projects the physician shortage will worsen materially over the next five years, which means AI-enabled diagnostic tools are becoming operational necessities for hospitals, not discretionary line items. GEHC is building the tools that healthcare systems will need to maintain care quality with fewer physicians, and that demand is structural. The opportunity is further concentrated in GEHC’s core domain: according to Research and Markets, radiology currently accounts for 77% of all AI medical device approvals, meaning the vast majority of healthcare AI innovation is happening in exactly the imaging and diagnostics categories where GEHC holds market leadership. GEHC is not a generalist hoping to benefit from AI; it dominates the specific vertical where AI adoption is most advanced. The radiologist shortage is also a global phenomenon: the UK currently faces a 30% shortage of clinical radiologists that is expected to widen to 40% by 2028, according to the 2026 AI in Breast Imaging Market report. This creates worldwide demand for AI-enabled imaging tools that function as a force multiplier, automating routine reporting, triaging scans to flag high-risk anomalies, and enabling accurate diagnoses despite rising case volumes. That same report found that AI tools can increase radiologist interpretation speeds by approximately 35%, the kind of concrete operational value that drives hospital purchasing decisions and commercial agreements. GEHC’s approach to capturing this market is worth noting: rather than selling standalone AI software, the company embeds advanced analytics directly into its existing radiology reading environments through OEM alliances, allowing providers to access AI capabilities without fragmented third-party software. This integrated approach deepens switching costs and locks AI revenue into the existing installed base rather than creating a separate product line vulnerable to competition.

Precision Medicine & Theranostics

The shift from one-size-fits-all medicine to precision diagnostics and targeted therapies is a multi-decade trend that directly benefits GEHC. The company’s Pharmaceutical Diagnostics segment, which grew 22.3% in Q4 2025, is at the forefront of this trend with Flyrcado (flurpiridaz F-18), the first and only FDA-approved F-18 PET myocardial perfusion imaging tracer for coronary artery disease. This product alone has a $500M+ annual revenue opportunity and positions GEHC as a leader in the expanding nuclear medicine and theranostics market. But Flyrcado is just the most visible piece of a broader precision care strategy. The January 2026 Deals and Alliances Profile documents GEHC’s systematic expansion into high-growth clinical areas: in oncology, co-development and licensing agreements with SOFIE Biosciences, Profound Medical, and Lantheus are expanding GEHC’s diagnostic imaging agents and radiotherapy tool capabilities. In cardiology, investments in Laza Medical and partnerships with DeepCardio and Boston Scientific are modernizing cardiovascular monitoring and treatment through AI-assisted data management and surgical guidance. These are the two highest-margin, fastest-growing clinical verticals in healthcare, and GEHC is building integrated diagnostic-to-treatment platforms across both.

Hospital Capital Spending Cycle

U.S. hospital capital spending is in a healthy expansion cycle. Hospital balance sheets have recovered from COVID-era disruptions, elective procedure volumes are at or above pre-pandemic levels, and health systems are investing in technology refresh cycles. Hospital patient volumes are climbing broadly, driving a 6.4% increase in healthcare spending in the current period per Research and Markets—a tailwind that flows directly into demand for GEHC’s installed base refresh and new system placements. GEHC’s record $21.8 billion backlog and consistent 1.06-1.09x book-to-bill ratios confirm that the capital equipment environment remains healthy. Emerging markets (Indonesia, India, Middle East) are also investing heavily in healthcare infrastructure, creating new demand for GEHC’s installed base.

BUSINESS OVERVIEW & SEGMENT DEEP DIVE

GE HealthCare operates four reportable segments, each serving distinct but interconnected healthcare needs. The company serves customers in over 160 countries with approximately 54,000 employees, including 11,100 engineers and scientists and approximately 9,800 sales professionals and 8,300 field service engineers. The company has over 5 million installed units globally, serving approximately 1 billion patients annually.

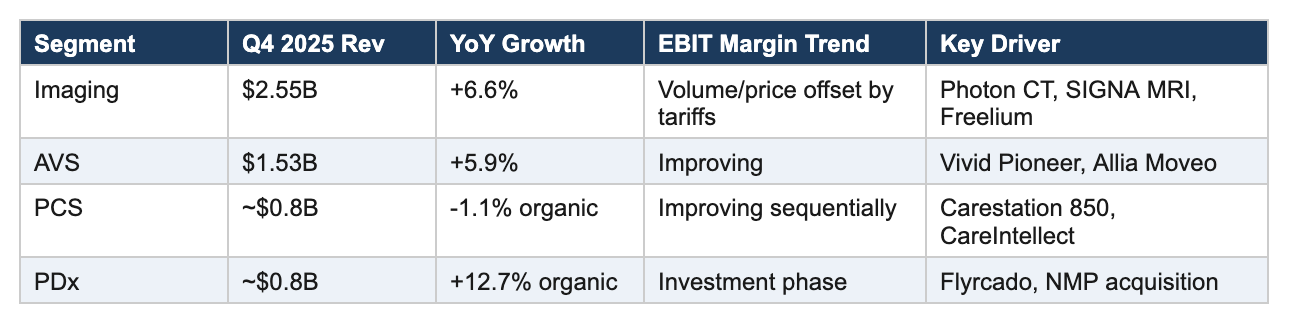

Segment 1: Imaging (~47% of Revenue)

The Imaging segment is the largest and most iconic business within GEHC. It encompasses five product lines: Molecular Imaging (MI), Computed Tomography (CT), Magnetic Resonance (MR), Women’s Health, and X-ray. Q4 2025 Imaging revenue was $2.55 billion, up 6.6% year-over-year, with full-year revenue representing the backbone of the enterprise. Key growth drivers include the photon-counting CT submission (on track for 2026 FDA approval), next-generation SIGNA MRI systems, the Freelium sealed magnet platform that uses less than 1% of traditional helium requirements, and the Omni Legend digital PET/CT scanner. One area that does not get enough attention from investors is the Women’s Health product line, where GEHC is profiled as a Key Player in the global AI in Breast Imaging Market—projected to grow from $320 million in 2025 to $441 million by 2031 at a 5.47% CAGR per the 2026 AI in Breast Imaging Market report. This growth is driven by the rising global incidence of breast cancer (an estimated 310,720 new invasive cases projected for US women in 2024 alone) and GEHC’s positioning in 3D mammography (tomosynthesis), where AI is increasingly used to analyze complex volumetric datasets, reduce false negatives, and improve detection rates in dense breast tissue. The FDA added 191 new AI-enabled medical devices in early 2024, with 128 specifically in radiology—and GEHC’s embedded AI approach means it captures this opportunity within its existing installed base rather than ceding it to third-party software vendors. EBIT margins in Imaging benefited from volume and price in Q4 but faced tariff headwinds.

Segment 2: Advanced Visualization Solutions (~27% of Revenue)

AVS provides ultrasound, image-guided therapies, and interventional solutions across clinical areas including women’s health, cardiovascular, and surgical visualization. Q4 2025 AVS revenue was $1.53 billion, up 5.9%. The segment recently launched the Vivid Pioneer, its most advanced AI-powered cardiovascular ultrasound system, and the Allia Moveo, a next-generation interventional imaging system that received both FDA 510(k) clearance and CE Mark. AVS represents a strong margin expansion opportunity as AI-enabled software layers drive mix improvement and recurring revenue.

Segment 3: Patient Care Solutions (~15% of Revenue)

PCS provides patient monitoring, diagnostic cardiology, anesthesia, respiratory care, and infant care devices. Q4 2025 organic revenue declined 1.1%, making this the weakest segment, though results improved sequentially after a Q3 product hold. EBIT margin improved 530 basis points sequentially but declined 380 bps year-over-year. Management views PCS as a turnaround opportunity, and the product pipeline supports that view. New launches include the Carestation 850 anesthesia delivery system, CareIntellect for Perinatal, and Portrait Mobile—a wireless wearable vital signs monitoring system released in 2023 that allows hospital patients full mobility while clinicians track respiration and heart rates in real-time. Portrait Mobile is the kind of product that shifts PCS from commodity monitoring hardware toward differentiated, software-enabled patient care. Worth flagging: a February 2026 Research and Markets report on the US neonatal monitoring market identifies GEHC as one of the four dominant companies in neonatal incubators and warmers alongside Draeger and Hill-Rom, positioning it to capture growth in a market segment with a long runway forecasted through 2033. The aging population gets all the attention from investors, but neonatal care is a durable, high-acuity niche where GEHC’s installed base and clinical relationships create real competitive advantages. PCS also has the highest recurring revenue mix of any segment, which supports earnings stability and positions it as a margin expansion contributor as new products scale.

Segment 4: Pharmaceutical Diagnostics (~11% of Revenue, but Highest Growth)

PDx is the growth engine of GEHC and arguably the single most undervalued asset within the business. Q4 2025 organic sales surged 12.7%, and the segment grew 22.3% on a reported basis—a medtech segment growing at software-like rates. PDx supplies contrast media and radiopharmaceuticals to the radiology and nuclear medicine industries. The segment’s crown jewel is Flyrcado (flurpiridaz F-18), the first and only FDA-approved F-18 PET myocardial perfusion imaging agent for coronary artery disease. Flyrcado is outperforming expectations. Dose delivery is running at approximately 220 per week with 95% on-time rates, and clinical adoption is accelerating as cardiologists experience the superior image quality firsthand. We model a credible path to $500 million in annual revenue by 2028, which would make Flyrcado one of the most successful diagnostic tracer launches in history. At current multiples, the market is assigning essentially zero incremental value to this product. PDx’s growth story also extends well beyond Flyrcado. The Nihon Medi-Physics acquisition strengthens GEHC’s foothold in the Asian radiopharmaceutical market, creating geographic diversification for a segment that is already the company’s fastest-growing. IBISWorld identifies this as part of GEHC’s broader ‘precision care’ strategy—systematically acquiring smaller, innovative manufacturers in molecular imaging and diagnostics where legacy competitors have been slow to adapt. The January 2026 Deals and Alliances Profile further reveals the depth of GEHC’s radiopharmaceutical pipeline beyond these headline acquisitions: investments in Nucleus RadioPharma and licensing agreements with Daiichi Sankyo for diagnostic imaging agents are building a global precision medicine platform that spans the full value chain from development through manufacturing and distribution. This is a systematic buildout of a radiopharmaceutical franchise with multiple shots on goal, not a one-product story. EBIT margins declined 330 bps in Q4 due to planned NPI investments and acquisition impacts, but this is intentional spending that seeds future profitability as the fixed-cost manufacturing base leverages against a rapidly growing volume base. PDx is GEHC’s highest-margin segment and the fastest growing.

Revenue Mix: Product vs. Service

GEHC generates approximately 50% of revenue from recurring sources (service contracts, consumables, software subscriptions) and is targeting 60% recurring revenue over time. In FY2025, product revenue grew 4.5% and service revenue grew 5.6%. The service business is higher-margin and lower-cyclicality, providing earnings stability and predictability. The Intelerad acquisition ($2.3B, expected H1 2026 close) will accelerate the shift toward cloud-based recurring SaaS revenue.

TAM, SAM, SOM & MARKET DYNAMICS

Total Addressable Market

GEHC’s Total Addressable Market spans multiple interconnected healthcare technology markets. The global medical imaging equipment market represents approximately $44 billion today, growing to $65-68 billion by 2032-2033. The in-vitro diagnostics and pharmaceutical diagnostics market adds another $10+ billion. Patient monitoring and clinical IT represent $15+ billion. The healthcare AI market is projected to reach $45-50 billion by 2030. In aggregate, GEHC’s TAM exceeds $100 billion globally. With $20.6 billion in 2025 revenue, GEHC has approximately 20% penetration of its broadest TAM. The US market alone represents a $58 billion opportunity per Research and Markets, and GEHC generated $8.6 billion in US industry-specific revenue in FY2025—a dominant position that provides operating leverage as healthcare spending growth (currently running at 6.4% annually) drives procedure volumes higher across the installed base.

Competitive Intensity & Barriers to Entry

The medical imaging market is an oligopoly dominated by three global players: GE HealthCare, Siemens Healthineers, and Philips. These three companies control approximately 70%+ of the global market. IBISWorld’s 2025 report pegs GEHC as the third-largest player in the US medical device market with a 14.8% market share, a position that delivers significant economies of scale in procurement, manufacturing, R&D amortization, and service network coverage. A significant contributor to GEHC’s depressed multiple is fear of low-cost Chinese hardware competition, and in our view, this fear is dramatically overstated. The barriers to entry in high-acuity medical imaging are steep to the point of being prohibitive. Regulatory barriers alone require FDA 510(k)/PMA clearances and global certifications that take 2-5+ years. The capital intensity requires billions in R&D spending. Installed base advantages create service revenue moats, and switching costs are extremely high because hospitals build workflows around specific platforms. Distribution and service networks of thousands of field engineers cannot be replicated quickly. And clinical evidence and trust built over 130 years cannot be commoditized. Chinese competitors like Mindray and United Imaging are gaining share in commodity modalities domestically, but they remain subscale globally and years away from competing in premium imaging where the margins live. IBISWorld further notes that large manufacturers like GEHC are better equipped to absorb tariff-related input cost increases through bulk purchasing and shifting production to tariff-exempt jurisdictions. Mexico now accounts for 17.3% of all US medical device imports per Research and Markets, and GEHC’s scale gives it flexibility to reroute supply chains in ways that smaller competitors simply cannot. The report also emphasizes that GEHC’s established brand name and clinical performance make its products ‘sticky,’ as hospital buyers are less likely to switch to cheaper, unfamiliar imports. Beyond scale, GEHC’s M&A strategy has built what industry analysts describe as a ‘protected base of demand’—an extensive patent portfolio and vertically integrated technology stack that prevents new entrants from easily replicating its capabilities across imaging, diagnostics, and clinical software. More importantly, the market’s fixation on hardware competition misses the real story: GEHC is actively shifting its business model away from commodity hardware exposure and toward software, AI, and diagnostics where Chinese competitors have no foothold at all. The Intelerad acquisition, Flyrcado, and CareIntellect AI platform are all moves that make the cheap-hardware-competition bear case increasingly irrelevant to the earnings trajectory.

Cyclicality Assessment

Medical imaging is moderately cyclical, with hospital capital budgets influenced by reimbursement changes, operating margins, and credit availability. That said, several factors dampen cyclicality: approximately 50% of revenue is recurring through service contracts and consumables, the aging installed base drives replacement demand regardless of the macro environment, backlog provides revenue visibility, and healthcare spending is structurally growing as a percentage of GDP. GEHC’s current $21.8B record backlog provides 12+ months of revenue visibility.

Bottom line on competitive positioning: this is a structurally advantaged franchise, not a fragile one. Oligopolistic market structure, massive installed base, regulatory moat, switching costs, and a recurring revenue shift create a durable business trading at a significant discount to intrinsic value.

BUSINESS MODEL MECHANICS & UNIT ECONOMICS

Revenue Drivers

GEHC’s revenue is driven by three levers: volume (new installations and replacement cycles), pricing (mix-up to premium AI-enabled systems), and recurring revenue (service contracts, consumables, software subscriptions). In FY2025, product revenue grew 4.5% and service revenue grew 5.6%, demonstrating balanced growth across both dimensions. The 55% three-year vitality rate—meaning 55% of revenue comes from products launched in the last three years, up ~5 percentage points—signals that new product introductions are increasingly contributing to the top line and commanding premium pricing.

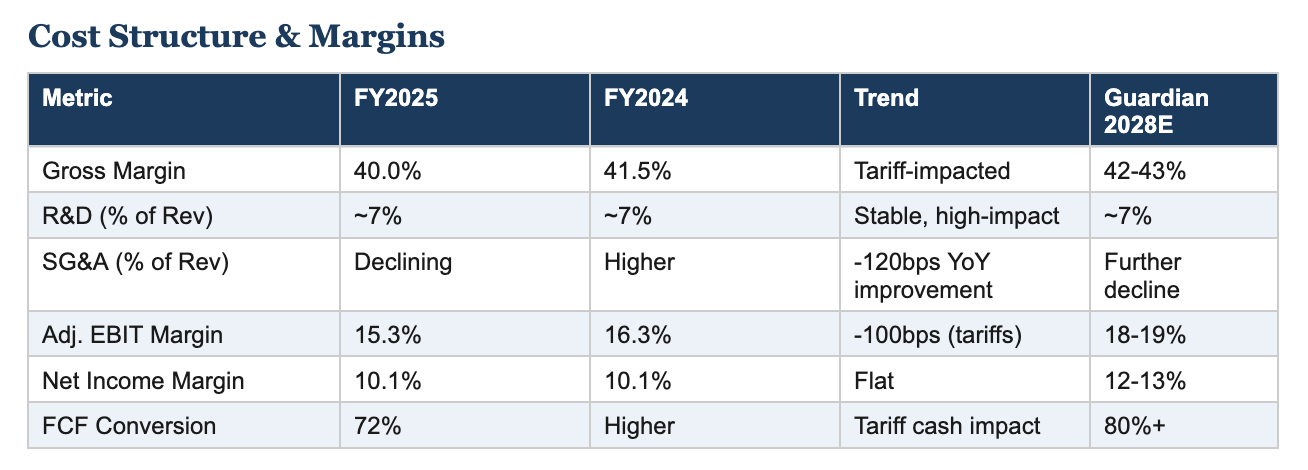

Incremental Margins & Margin Expansion Runway

This is where the real story lives. GEHC’s current 15.3% adjusted EBIT margin is depressed by three transient factors: (1) $245 million in tariff costs in FY2025 that will diminish; (2) intentional investment spending on NPI launches and acquisitions; and (3) China-related volume weakness. Excluding tariffs alone, EBIT margin would have expanded 20 bps in FY2025. Looking forward, the Heartbeat lean system is driving measurable operational improvements—a 25% reduction in past-due backlog, AI-driven sales efficiency with 80% of managed leads handled by AI, and engineering productivity up 25% through AI coding tools. Management is guiding 50-80 bps of margin expansion in 2026. We model 200+ bps of cumulative margin expansion over 2026-2028, driven by Heartbeat deployment, new product mix-up, tariff mitigation, and SG&A leverage.

Revenue Quality

GEHC’s revenue quality is improving in ways the Street has not fully priced in. Approximately 50% of total revenue is now recurring (services, consumables, diagnostics agents), up from historical levels, with a clear target of 60%. This shift matters: recurring revenue is higher-margin, more predictable, and commands materially higher valuation multiples from the market. The Intelerad acquisition ($270M revenue growing low double-digits, EBITDA margins above 30%) is the deal that fundamentally accelerates the transformation from a cyclical hardware business into a recurring-revenue platform company. Intelerad brings cloud-native enterprise imaging software with long-term SaaS contracts, sticky hospital relationships, and the kind of predictable revenue stream that gets valued at 8-12x sales in the software world versus 2-3x for equipment. Every dollar of lumpy capital equipment revenue that gets replaced or augmented by recurring SaaS and diagnostics revenue structurally re-rates the earnings multiple the market will pay for this business. Customer concentration risk is low—GEHC serves thousands of hospitals and health systems globally with no single customer representing a material percentage of revenue.

COMPETITIVE MOAT ANALYSIS

Not just a strong brand. Let us break down GEHC’s moat layer by layer.

1. Economies of Scale

At $20.6 billion in revenue, GEHC is one of two companies globally (alongside Siemens Healthineers at ~$23B) with the scale to amortize R&D spending of $1.7+ billion annually across a global installed base. Smaller competitors cannot match this R&D intensity. Scale drives purchasing power with suppliers, manufacturing efficiency, and global service coverage that smaller players simply cannot replicate.

2. Switching Costs (Very High)

Hospitals build entire clinical workflows, training programs, and IT integrations around their imaging platform vendor. Switching from GE to Siemens or Philips requires retraining radiologists and technologists, reconfiguring PACS and IT systems, renegotiating service contracts, and accepting workflow disruption during transition. The total cost of switching is measured in millions of dollars and months of disruption. The result is extreme customer stickiness—once you are in a hospital’s imaging department, you tend to stay for decades.

3. Regulatory Moat

Medical devices require FDA 510(k) or PMA clearances in the U.S. and equivalent approvals in 160+ countries. GEHC has 130 years of regulatory history and the institutional knowledge to navigate these processes efficiently. New entrants face years of regulatory development before they can sell a single unit. On top of that, GEHC leads the industry with 80+ FDA-cleared AI algorithms, creating a compounding regulatory advantage as each cleared algorithm extends the platform.

4. Installed Base & Distribution Dominance

With 5+ million units installed globally and a network of 8,300+ field service engineers, GEHC’s installed base is a self-reinforcing competitive advantage. Each installed unit generates recurring service revenue for 10-15+ years, creates upgrade and replacement opportunities, and reinforces vendor lock-in. The service network itself is a moat—hospitals need 24/7 service support for critical medical equipment, and building a global field service organization of this scale requires decades and billions of dollars.

5. Data Advantage

GEHC’s installed base generates an enormous volume of clinical imaging data that feeds its AI development pipeline. More data leads to better AI models, which leads to better clinical outcomes, which drives more sales and more data—a classic data flywheel. With 1 billion patients served annually, GEHC has access to clinical data at a scale that no startup or smaller competitor can match.

6. Network Effects (Emerging)

The CareIntellect platform and Genesis Radiology Workspace are creating network effects in clinical software. As more hospitals adopt GEHC’s cloud-based platforms, the value of the network increases through shared clinical insights, workflow benchmarking, and AI model improvements. The Intelerad acquisition amplifies this by adding enterprise imaging capabilities across outpatient networks.

7. Embedded AI Distribution Advantage

A moat layer that deserves more attention is GEHC’s OEM embedding strategy for AI. The 2026 AI in Breast Imaging Market report identifies a key industry trend: the formation of strategic alliances between AI vendors and imaging OEMs like GEHC. Rather than selling standalone AI software that competes on a level playing field with startups, GEHC embeds advanced analytics directly into its existing radiology reading environments. This means hospitals can access AI capabilities without purchasing fragmented third-party software, and it means AI revenue flows through GEHC’s existing customer relationships rather than creating new competitive entry points. The report also notes that early AI adoption is concentrated in well-funded academic medical centers and large health systems—exactly the institutions where GEHC’s installed base is most deeply entrenched. Smaller practices face higher barriers to AI adoption due to implementation costs, which means the initial wave of AI spending disproportionately flows to GEHC’s core customer base. As AI capabilities mature and costs decline, GEHC can then push these tools downstream to community hospitals already on its platform.

Moat Trajectory: Widening

GEHC’s moat is widening on multiple fronts simultaneously. The combination of AI leadership (80+ FDA clearances, partnerships with NVIDIA, Intel, and dozens of specialist AI firms), Heartbeat operational improvements, the Intelerad cloud platform acquisition, Flyrcado PDx expansion, and an accelerating deal pipeline ($5.07B deployed in 2025 alone) are all accretive to the competitive position. The company is investing $1.7B+ annually in innovation while simultaneously improving operational efficiency—the hallmark of a widening moat.

MANAGEMENT QUALITY & CAPITAL ALLOCATION

A. Management Quality Assessment

CEO Peter Arduini: Arduini is a medtech veteran who spent his formative years at GE under Jack Welch, left in 2005, and was recruited back by Larry Culp to lead the healthcare spinoff. He brings deep domain expertise from leadership roles at Integra LifeSciences (CEO) and Baxter International. His Fortune interview reveals a leader who is deliberately reviving GE’s legendary management development systems while maintaining the agility of a focused company. Arduini directly owns approximately 164,672 shares. His compensation is heavily weighted toward performance-based equity tied to EPS and organic revenue targets through 2026.

CFO Jay Saccaro: Previously CFO of Baxter International, Saccaro brings disciplined financial management and has been instrumental in strengthening the balance sheet through $250M+ in annual debt repayment while simultaneously increasing R&D investment. His communication on earnings calls is clear, detailed, and credibly conservative.

Chairman Larry Culp: The architect of the GE transformation, Culp serves as non-executive Chairman. His involvement provides strategic continuity and investor confidence. An independent Lead Director (Risa Lavizzo-Mourey) and fully independent committees provide governance rigor.

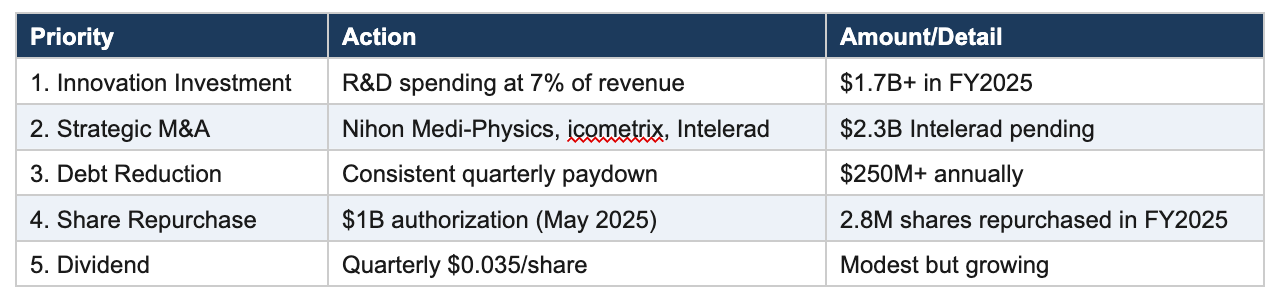

B. Capital Allocation Track Record

Since the January 2023 spinoff, GEHC has demonstrated a disciplined capital allocation framework that balances reinvestment, M&A, debt reduction, and shareholder returns:

The scope and velocity of GEHC’s deal-making since independence tells a story that the quarterly earnings alone do not capture. According to the January 2026 GE HealthCare Deals and Alliances Profile, the company has been on a sustained expansion campaign: deal activity peaked in 2022 at 28 transactions valued at $9.37 billion, maintained at $3.49 billion across 2024, and accelerated again in 2025 with 10 deals totaling $5.07 billion. Management is clearly not optimizing for near-term EPS here. They are investing aggressively to build a platform for the next decade of growth. The deal pipeline spans three strategic vectors that each reinforce the others:

AI and Digital Infrastructure: GEHC has assembled a formidable ecosystem of AI partnerships that extends well beyond internal R&D. The Deals and Alliances Profile documents collaborations with NVIDIA and Intel to build high-performance AI-driven diagnostic infrastructure, partnerships with MediView XR, Caption Health, Arterys, and Sophia Genetics to embed advanced analytics into imaging workflows, and agreements with Therapixel (MammoScreen) for AI-powered breast cancer screening. These go beyond press-release partnerships. They are integrations that make GEHC’s hardware platform the operating system for healthcare AI, deepening the moat with every new alliance.

Oncology and Cardiology Expansion: The company has entered numerous co-development and licensing agreements in high-growth clinical verticals. In oncology, partnerships with SOFIE Biosciences, Profound Medical, and Lantheus Medical Imaging expand GEHC’s diagnostic imaging agents and radiotherapy capabilities. In cardiology, investments in Laza Medical and partnerships with DeepCardio and Boston Scientific are modernizing cardiovascular monitoring and treatment through better data management and AI-assisted surgical guidance. These are the highest-margin, fastest-growing clinical areas in healthcare, and GEHC is building positions across all of them.

Global Radiopharmaceutical Leadership: Beyond Flyrcado, GEHC is systematically building a radiopharmaceutical franchise through investments in Nucleus RadioPharma and licensing agreements with Daiichi Sankyo for diagnostic imaging agents. Combined with the Nihon Medi-Physics acquisition in Asia, GEHC is constructing a global precision medicine platform that spans development, manufacturing, and distribution—the kind of vertically integrated radiopharm capability that very few companies in the world can replicate.

C. ROIC vs. WACC

GEHC’s return on invested capital stands at approximately 14.2%, which exceeds its estimated WACC of 8-9%. This positive ROIC-WACC spread indicates that every incremental dollar of reinvestment creates value—and this is the foundation of the 5-year compounding thesis. As margins expand from 15.3% toward 19-20% and the Intelerad/Flyrcado investments mature, we expect ROIC to trend toward 18-22% by 2030, dramatically widening the value creation spread. A company compounding capital at 18-22% returns in a sector trading at 35x earnings should not be available at 16x. The market will eventually close this gap, and the 20% IRR we project is the mathematical consequence of that normalization.

Would you trust this CEO with permanent capital? We would. Arduini’s track record of focused execution, his alignment through equity ownership, the 92.6% say-on-pay approval, and the disciplined capital allocation framework all support confidence in management. The Heartbeat lean system is institutional, not personality-dependent, reducing key-person risk.

EARNINGS GROWTH RUNWAY: THE UNDERESTIMATED STORY

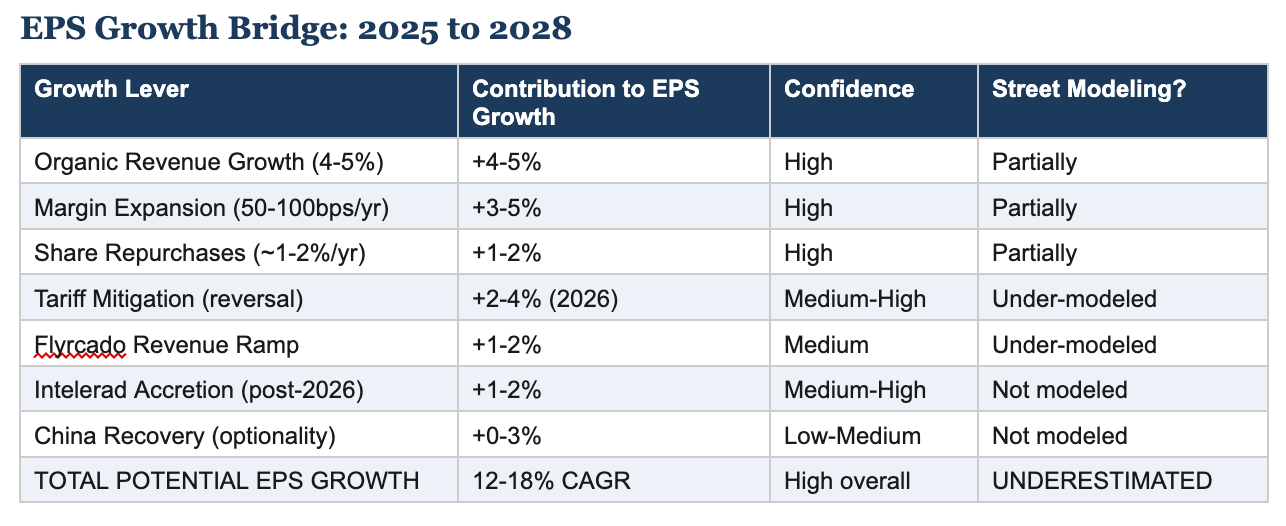

THIS IS THE CORE OF OUR THESIS. Wall Street is modeling mid-single-digit EPS growth. We see a clear path to sustained 12-18% EPS CAGR through 2028, driven by compounding levers that consensus has not fully modeled.

Why Wall Street Is Wrong

Consensus models GEHC growing adjusted EPS at roughly 8-10% annually. The Street is anchored to the company’s 2024-2025 results, which were significantly depressed by tariff headwinds that the Street assumes persist. Here is what the consensus is missing:

First, tariff headwinds are peaking, not persisting. In FY2025, tariffs reduced adjusted EPS by $0.43 and EBIT by $245 million. Management has already mitigated approximately 50% of gross tariff exposure through USMCA compliance, supply chain shifts, and supplier negotiations, and expects 2026 tariff impact to be lower than 2025. By 2027-2028, tariff mitigation should be substantially complete, creating a significant earnings tailwind that is not in consensus models.

Second, the innovation renaissance is real and quantifiable. GEHC’s three-year vitality rate is 55%, up approximately 5 percentage points, meaning more than half of revenue now comes from products launched in the last three years. New products launch at higher prices and lower costs than their predecessors. The pipeline includes photon-counting CT (potential 2026 approval), next-gen SIGNA MRI, Freelium platform, Flyrcado, Vivid Pioneer, Allia Moveo, and multiple AI software platforms. This product cycle is the strongest in GEHC’s history and will drive both revenue acceleration and margin expansion.

Third, Heartbeat lean is systematically improving operations. The 25% reduction in past-due backlog is not a one-time event—it is the beginning of a multi-year operational improvement cycle that will drive SG&A leverage, manufacturing efficiency, and cash flow conversion. AI-driven productivity gains (80% of leads handled by AI, 25% engineering productivity improvement) compound over time.

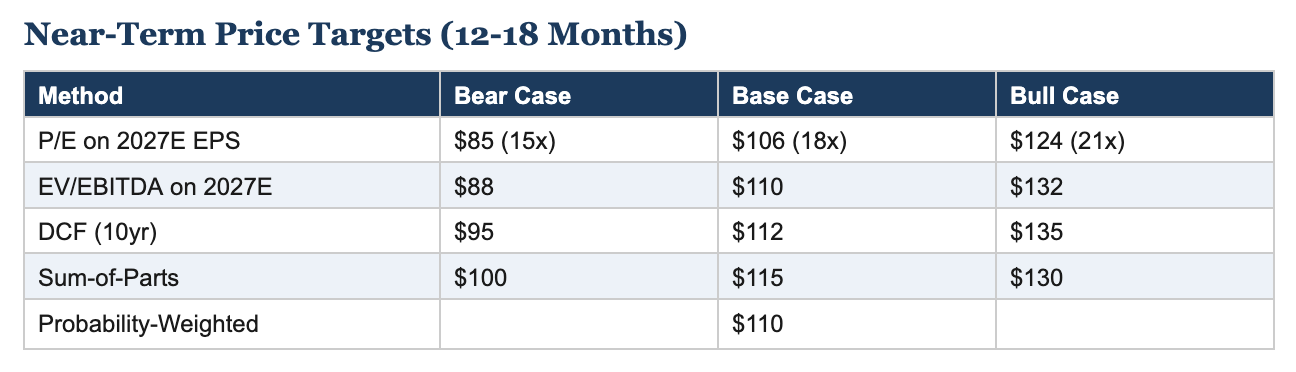

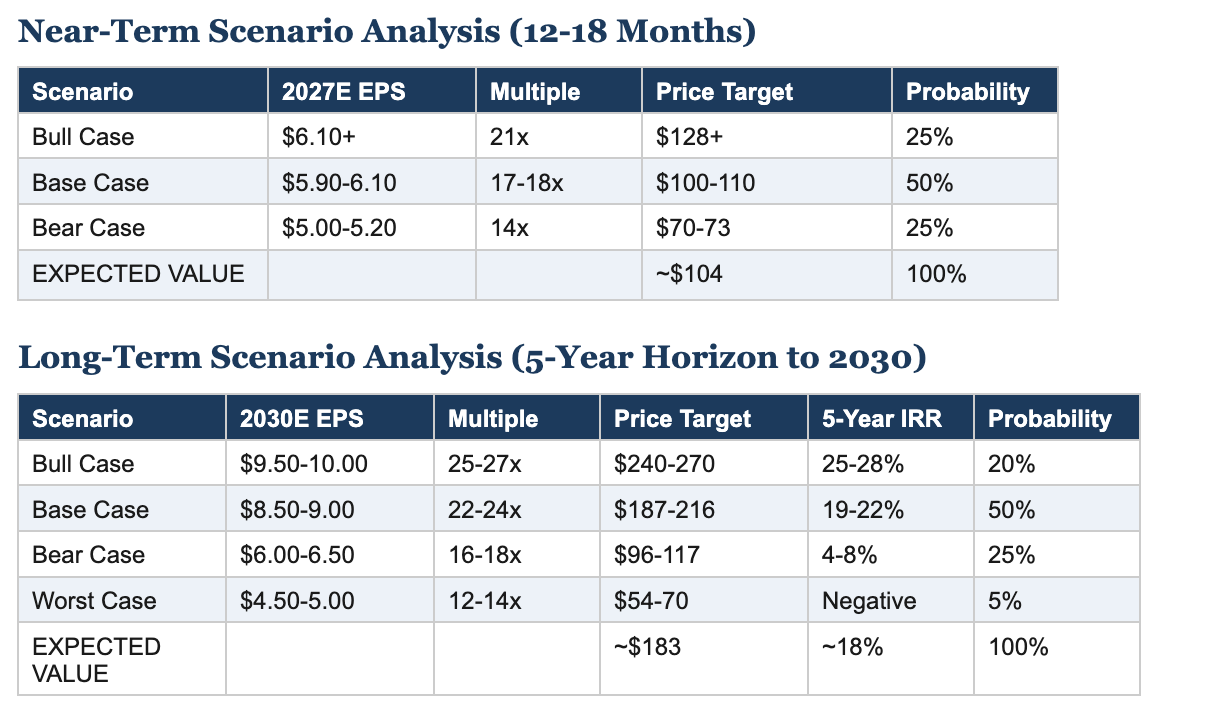

The Math — Near-Term: At $6.00-6.50 in 2027E EPS and a 17-18x P/E (still below medtech averages), GEHC is worth $102-117 per share. Our near-term target of $110 is achievable as soon as the market prices in the earnings inflection. The Math — Long-Term: If EPS compounds at 15-18% annually through 2030, reaching $8.50-9.50, and the multiple re-rates to just 22-24x (still a significant discount to the 35x medtech peer average) as the recurring revenue mix shift becomes undeniable, GEHC reaches $187-228 per share. Our $200 long-term target sits in the middle of this range and delivers a 20.11% annualized IRR over 5 years. None of this requires heroic assumptions. It just requires the market to start pricing this business for what it actually is.

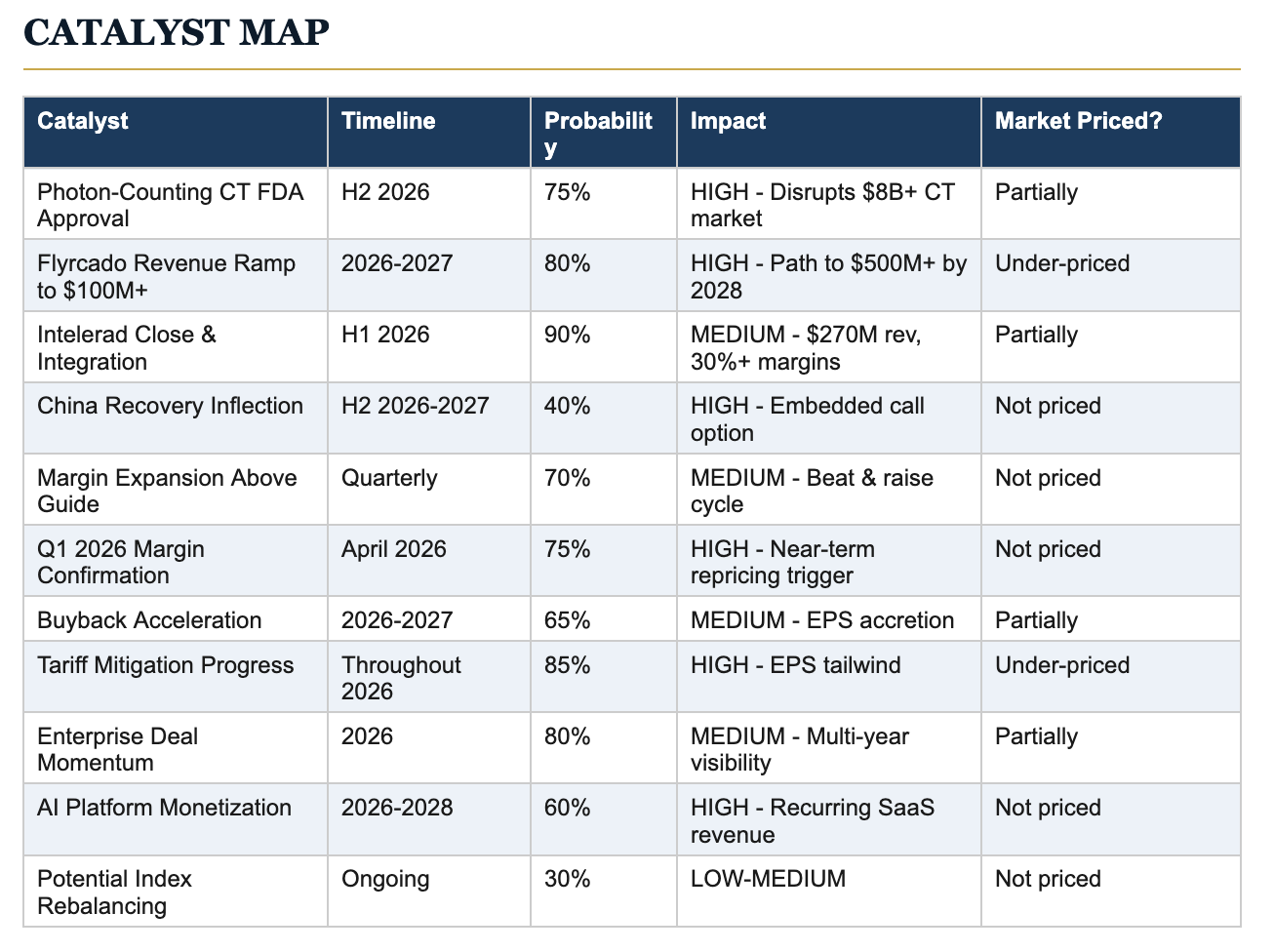

Of the catalysts listed, we want to draw particular attention to Q1 2026 earnings as a near-term inflection point for the stock. If management delivers margin expansion in line with or above their 50-80 bps annual guide in the first quarter, it will validate the Heartbeat lean thesis and signal that the tariff headwind is genuinely fading. The market is skeptical—consensus is modeling conservative margins—so a clean Q1 print with margin expansion would force a rapid repricing into the $90s as institutional models get revised upward. This is the kind of catalyst where patience over the next 60-90 days gets rewarded disproportionately.

Q3 & Q4 2025 EARNINGS DEEP DIVE

Q4 2025 Results (Reported February 4, 2026)

GEHC delivered a strong Q4 that beat expectations on both revenue and earnings. Revenue came in at $5.70 billion, up 7.1% reported and 4.8% organic, beating consensus of $5.60 billion by 1.7%. Adjusted EPS of $1.44 beat the $1.40 consensus by 3%. The quarter was characterized by double-digit organic growth in Pharmaceutical Diagnostics (+12.7%), mid-single-digit growth in Imaging (+5.3% organic) and AVS, and continued strength in U.S. and EMEA markets. The record $21.8 billion backlog grew $2 billion year-over-year and $600 million sequentially. Book-to-bill was 1.06x. Free cash flow was $916 million, up $105 million year-over-year.

The visual tells the story better than any table: GEHC has beaten EPS expectations in every single quarter since Q3 2024, with the magnitude of beats accelerating—from a 9% beat in Q3 2024 to a 15% beat in Q4 2024, then sustained beats through 2025 culminating in a 3% beat on higher expectations in Q4. Revenue has followed the same pattern, beating estimates in four of the last six quarters. This is a management team that under-promises and over-delivers, and investors who fade the guidance are consistently leaving money on the table. The dashboard also highlights the quality metrics that underpin the thesis: a 40.8% gross profit margin, 17.9% EBITDA margin, and 24.78% ROE—profitability metrics that compare favorably to medtech peers yet command a fraction of the valuation. The P/E of 16.6x at $78.79 is the number that should jump off the page: this level of earnings quality and growth consistency trading at a discount to the S&P 500 is the mispricing opportunity.

The key negative was margin pressure: adjusted EBIT margin of 16.7% was down 200 bps year-over-year, driven by approximately $100 million in tariff expense and unfavorable mix. But management specifically noted that excluding tariffs, adjusted EPS would have grown 11% and margins would have expanded. That distinction matters a lot for understanding the underlying earnings power.

Q3 2025 Results

Q3 2025 showed similar dynamics. Revenue of $5.1 billion grew 6% reported and 4% organic, beating expectations. Orders surged 6% organically with growth across all segments. Backlog reached $21.2 billion. Adjusted EBIT margin was 14.8%, down 150 bps due to $95 million in tariff costs. The tell was that management raised the lower end of full-year EPS guidance after Q3, signaling confidence in underlying execution. The Vivid Pioneer cardiovascular ultrasound and Carestation 850 anesthesia system were launched during the quarter.

Earnings Call Key Takeaways

From the Q4 2025 earnings call, several things stood out. First, 2026 guidance of $4.95-$5.15 adjusted EPS beat consensus of $4.93, signaling management confidence. Second, China is being guided down prudently—management assumes a decline in China for 2026 despite seeing improved VBP win rates, better imaging funnel, and tender wins. Third, Flyrcado is delivering approximately 220 doses per week with 95% on-time delivery, tracking toward revenue acceleration. Fourth, the Intelerad acquisition is not included in 2026 guidance, representing pure upside optionality. And fifth, Heartbeat deployment drove a 25% improvement in past-due backlog, demonstrating operational momentum.

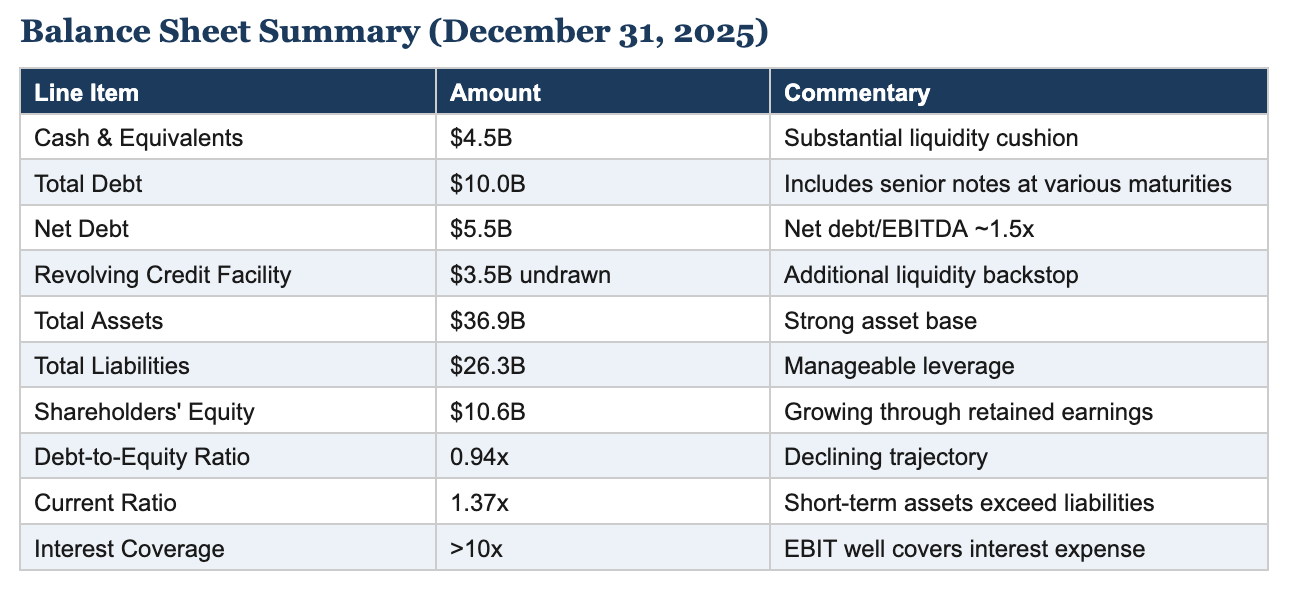

BALANCE SHEET DEEP DIVE

Understanding the balance sheet is essential for assessing financial risk and capital allocation flexibility. GEHC entered public life with a levered balance sheet inherited from the GE spinoff, and management has been systematically strengthening it.

Debt Maturity Profile

GEHC’s debt is well-laddered across multiple maturities reaching as far as 2052, reducing refinancing risk. The January 2026 Deals and Alliances Profile details the company’s sophisticated capital markets execution: GEHC has successfully priced multiple senior note offerings ranging from $600 million to $1.75 billion across various maturities, and raised billions through secondary share offerings in 2024 and 2025 including a $1.15 billion public offering and a $1.95 billion secondary offering. This capital markets access is a competitive advantage in itself—it signals strong investor demand and provides the liquidity runway to fund both the Intelerad acquisition and ongoing strategic investments without straining the balance sheet. The company has been paying down approximately $250 million annually in debt while simultaneously investing in growth. Investment-grade credit ratings provide access to capital markets at favorable rates. The planned $2.3 billion Intelerad acquisition will be funded with cash on hand and new debt, temporarily increasing leverage, but GEHC’s free cash flow generation of $1.5-1.7 billion annually provides a rapid delevering path.

Working Capital & Cash Conversion

FY2025 operating cash flow was $2.0 billion, and free cash flow was $1.5 billion, representing a 72% FCF conversion rate. Capital expenditures were approximately $482 million. The tariff environment created a $285 million cash headwind in FY2025 that depressed FCF conversion below normalized levels. Strip out the tariff distortion and normalized cash conversion is essentially dollar-for-dollar—every dollar of adjusted net income converts to free cash flow. That kind of earnings quality stands in stark contrast to peers where aggressive revenue recognition, channel stuffing, or heavy capitalization create a gap between reported earnings and actual cash generation. The cash conversion profile gives us high confidence in the durability of the earnings growth we are modeling. For 2026, management guides approximately $1.7 billion in FCF, representing 13% growth and improved conversion as tariff cash impacts moderate. We model FCF approaching $2.0-2.3 billion by 2028 as margin expansion, working capital optimization, and a growing share of recurring software revenue take hold.

Bottom line on the balance sheet: solid and improving. Net leverage of approximately 1.5x net debt/EBITDA is conservative for a stable healthcare franchise. The $4.5B cash position and $3.5B undrawn revolver provide ample liquidity for the Intelerad acquisition and ongoing investment. There is no near-term solvency concern.

VALUATION: COMPS, DCF & SCENARIO ANALYSIS

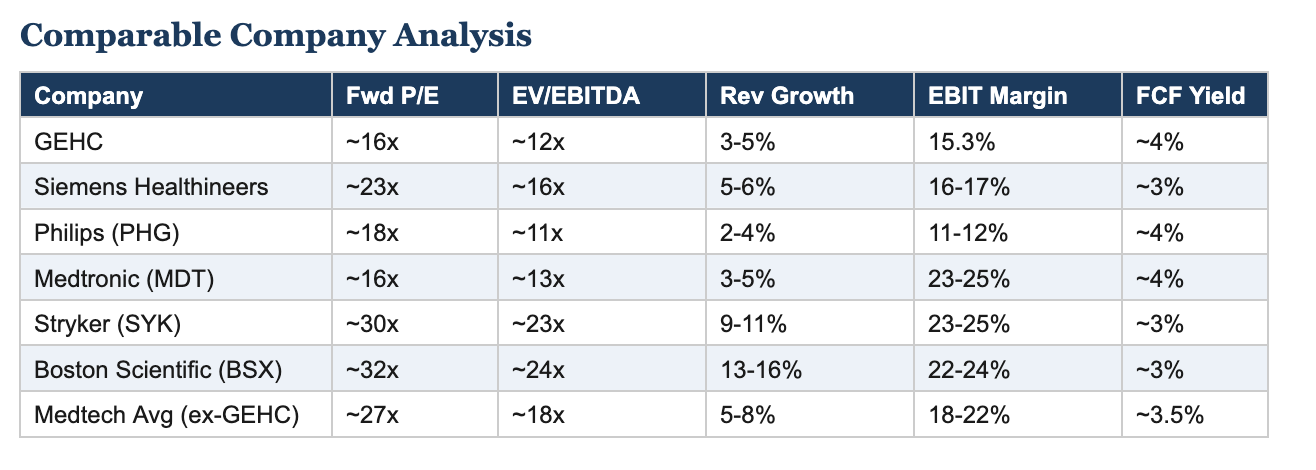

GEHC trades at approximately 16x forward P/E versus the medtech peer average of 27-37x. Even compared to Siemens Healthineers, its closest comparable, GEHC trades at a 30%+ discount. This discount reflects lingering GE conglomerate stigma, China concerns, and tariff-depressed margins. We believe this discount will narrow as GEHC demonstrates earnings acceleration, margin expansion, and a clean execution track record as an independent company.

DCF Analysis

Our base case DCF uses a 9.5% WACC and 2.5% terminal growth rate. With revenue growing at 5-6% annually (accelerating from organic growth plus Intelerad and Flyrcado contributions), EBIT margins expanding from 15.3% to 19-20% by 2030 as recurring revenue scales and Heartbeat lean compounds, and capex at approximately 2.3% of revenue, our near-term DCF derives a fair value range of $105-120 per share. Extending the model through 2030 with our full earnings trajectory—reflecting the business model transformation toward 60%+ recurring revenue—the 5-year DCF fair value rises to $175-210 per share. The DCF is highly sensitive to assumptions about terminal margin and terminal multiple: each 100 bps of additional margin expansion adds approximately $8-10 per share to intrinsic value, and each 1x turn of terminal multiple adds $12-15.

Sum-of-the-Parts Analysis

Valuing GEHC’s segments independently using segment-appropriate multiples yields an even higher value. Imaging at 14-16x EBIT, AVS at 16-18x, PCS at 12-14x, and PDx at 20-25x (reflecting its growth profile and Flyrcado optionality) sum to an enterprise value of $50-60 billion, implying a share price of $100-120. This approach highlights that the market is not properly crediting GEHC’s fastest-growing segment (PDx) within the blended multiple.

Long-Term Price Targets (3-5 Years)

The long-term return case for GEHC is built on a dual-engine framework: sustained double-digit EPS compounding combined with a structural re-rating of the earnings multiple as the business mix shifts toward recurring revenue.

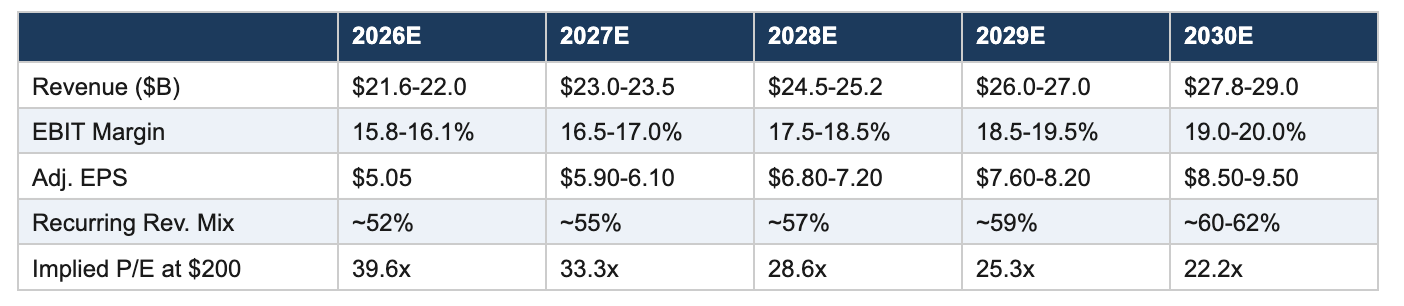

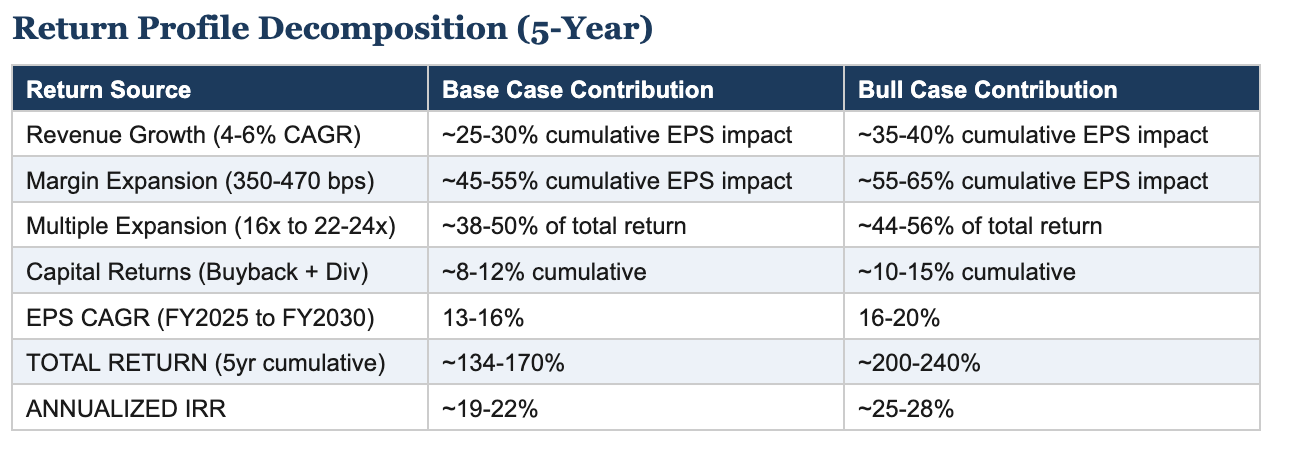

The EPS bridge from $4.59 in FY2025 to $8.50-9.50 by 2030 is supported by: organic revenue growth of 4-6% annually ($3-4B incremental revenue), margin expansion of 350-470 bps as Heartbeat lean compounds, tariffs fade, and the recurring revenue mix shifts toward 60%+ (each percentage point of mix shift toward software/services adds approximately 40-50 bps to blended margins), Intelerad accretion adding $0.15-0.25 of EPS annually by 2028, Flyrcado scaling to $500M+ in revenue at margins well above corporate average, share buyback accretion of 1-2% annually from the $1B authorization and growing free cash flow, and operating leverage inherent in a business with $1.7B+ of fixed R&D expense against a growing revenue base. The implied P/E at our $200 target in 2030 is approximately 22x, which is still a deep discount to where Siemens Healthineers (23x), Danaher (27x), and the broader medtech universe (35x) trade today. Put differently, our $200 target does not require GEHC to be valued in line with peers. It just requires the market to give it credit for what it is actually becoming.

Guardian Research Dual-Target Framework: Near-Term Target of $110 per share (~38% upside) as the market prices in the current earnings inflection—achievable on 18x 2027E EPS of $5.90-6.10. Long-Term Target of $200 per share (~150% total return, 20.11% annualized IRR over 5 years) as EPS compounds to $8.50-9.50 by 2030 and the multiple re-rates to 22-24x reflecting the recurring revenue transformation. Even at $200, GEHC would trade below the medtech peer average, meaning our long-term target embeds significant conservatism.

TECHNICAL ANALYSIS

GEHC’s technical setup supports the fundamental thesis. The stock is trading near $80, well below its 52-week high of $93.26 and above its 52-week low of $57.65. The current price represents a favorable risk/reward entry point for multiple reasons.

The chart tells a constructive story. After the sharp sell-off from the $90 area post-Q4 earnings spike in late January, GEHC has found support right at the rising 100-day simple moving average around $75-76. The stock is now consolidating in the $78-80 range—precisely at the horizontal support level (blue dotted line) that has acted as a pivot point throughout 2025. This is the kind of technical setup that swing traders look for: a stock pulling back to its moving average support after an impulse move higher, with the fundamental catalysts (Q1 margin confirmation) still ahead. The dividend payouts visible along the bottom of the chart also confirm the steady capital return program. The key levels to watch are all visible on this chart: the 100-day SMA providing dynamic support below, the $80 horizontal pivot acting as the current battleground, and the $88-90 area representing the next resistance zone that a Q1 earnings beat would likely push through.

Key Technical Observations

First, the stock has established strong support in the $75-80 zone, which served as resistance during the 2023 breakout and has now flipped to support. This area also coincides with the 200-day moving average, adding a layer of technical significance. Second, the RSI (14-day) is at approximately 64, indicating the stock is neither overbought nor oversold—a neutral positioning that suggests room for upside momentum. Third, the stock’s beta of 1.23 indicates slightly higher volatility than the market, which creates opportunity for active investors.

Fourth, volume patterns are constructive. The Q4 earnings report on February 4, 2026, produced a modest positive reaction as the stock rose in premarket trading on the beat-and-raise, suggesting institutional accumulation at these levels rather than distribution. Average daily volume of approximately 4.25 million shares provides ample liquidity.

The technical picture supports a long entry at current levels with a stop-loss consideration near $72-73 (below the 200-day MA and recent support), which would represent approximately 10% downside risk against 38% upside to our near-term $110 target. This creates a near-term asymmetric risk/reward ratio of approximately 3.8:1. On a long-term basis, the math is even more attractive: 10% downside to stop-loss versus 150% upside to our $200 five-year target.

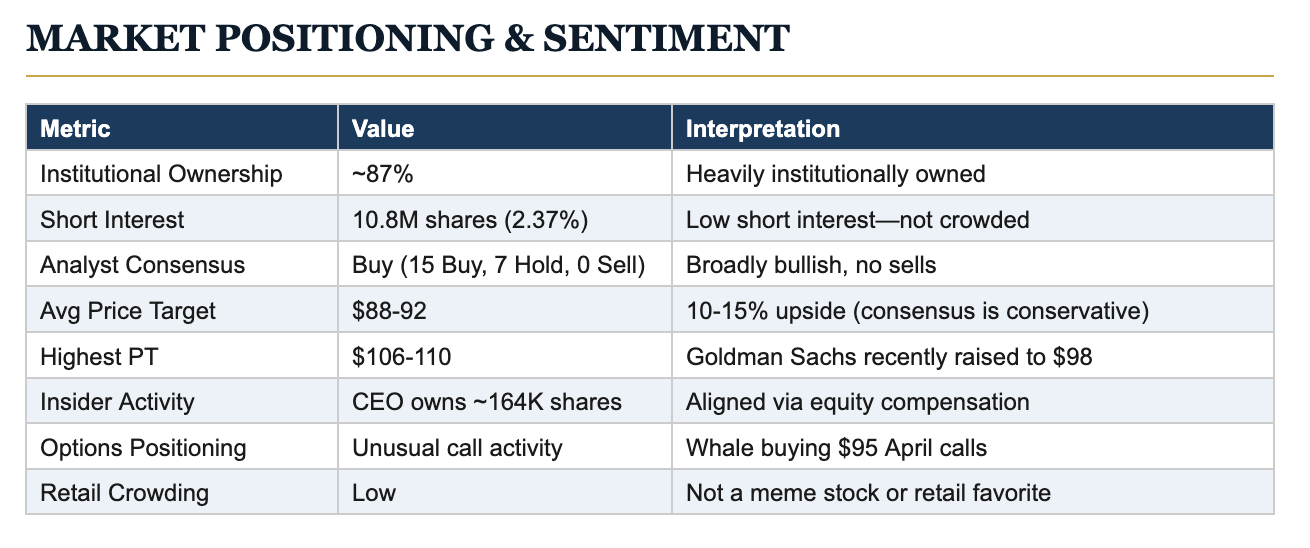

The sentiment setup is favorable for contrarian long investors. Institutional ownership is high (87%) but the stock is not over-owned relative to peers. Short interest at 2.37% is minimal—there is no significant short thesis to unwind, but also no short squeeze dynamic. Analyst consensus is bullish but conservative, with most price targets in the $85-98 range, well below our near-term $110 target and a fraction of our long-term $200 thesis. This creates multi-layered asymmetry: as analysts gradually revise estimates higher (as we expect), each upgrade cycle drives incremental re-rating. Goldman Sachs recently raised their target to $98, and Stifel raised to $98 post-Q4 earnings. Evercore ISI is at $98. These are moving in the right direction but still reflect only a fraction of the earnings compounding potential we model through 2030.

Smart Money Positioning: Unusual Options Activity

We are not the only ones positioning for this. The options market is signaling that informed capital is betting on a near-term move higher. On February 4, 2026, Unusual Whales flagged significant call option activity in GEHC that caught our attention. A large buyer purchased 1,301 contracts of the $95 strike calls expiring April 17, 2026, paying $1.10 per contract for a total premium outlay of approximately $143,000. That is a directional bet, not a hedge. The buyer needs GEHC above $96.10 by mid-April, which happens to be right around Q1 2026 earnings.

The timing is what makes this noteworthy. The April 17 expiry gives these contracts exposure to the Q1 2026 earnings report, which we have identified as the single most important near-term catalyst. If management delivers on the 50-80 bps margin expansion guide—which we believe is conservative—the stock reprices into the $90s as institutional models get revised upward. This whale is betting on the exact same catalyst we have been building the case for throughout this report. For a buyer to commit $143,000 in premium on short-dated, out-of-the-money calls, they are either seeing something in the data that the market has not priced in, or they share our conviction that the Q1 print will be a catalyst. Either way, when smart money aligns with our fundamental thesis and our catalyst timeline, it strengthens our confidence in the setup.

RISK ANALYSIS: HOW WE PERMANENTLY LOSE CAPITAL

Every position must answer: How do I permanently lose capital here? This section addresses that question with intellectual honesty.

Structural Risks

Technology disruption is a theoretical risk, but the medical imaging oligopoly has been remarkably stable for 30+ years. Chinese competitors (Mindray, United Imaging) are gaining share domestically but remain years away from competing globally at GEHC’s scale. AI could theoretically commoditize imaging interpretation, but GEHC leads in AI with 80+ FDA clearances, making it the beneficiary rather than victim of this trend.

Financial Risks

Leverage is moderate at approximately 1.5x net debt/EBITDA, and the Intelerad acquisition will temporarily increase it. However, GEHC’s $1.5-1.7B annual free cash flow provides rapid delevering capacity. Interest coverage exceeds 10x. There is no near-term debt maturity risk.

Execution Risk

The largest risk is execution failure on the innovation pipeline. If photon-counting CT is delayed, Flyrcado adoption is slower than expected, or Heartbeat operational improvements stall, the earnings acceleration thesis weakens. We assess this risk as manageable given management’s track record of under-promising and over-delivering (FY2025 beat initial guidance on all metrics).

China Risk

China represents approximately 10-12% of GEHC revenue and has been a headwind due to government volume-based procurement policies, geopolitical tensions, and slower economic recovery. Management is prudently assuming a decline in China for 2026. If China deteriorates further, it could reduce EPS by $0.10-0.20 versus our estimates. However, this risk is already embedded in guidance and the stock price.

Tariff Risk

Tariffs cost GEHC $245 million in EBIT and $0.43 in EPS in FY2025, and Research and Markets notes that tariffs on medical device components can exceed 30%—a significant headwind for any manufacturer without mitigation options. If tariffs escalate further, margins could compress. However, mitigation actions are well underway, and management expects 2026 impact to be less than 2025. Industry analysis confirms that large-scale device manufacturers like GEHC have a structural advantage in absorbing tariff shocks through bulk purchasing power and the ability to shift production to tariff-exempt jurisdictions. Mexico now accounts for 17.3% of all US medical device imports, and GEHC’s global manufacturing footprint provides nearshoring optionality that smaller competitors lack. Policy uncertainty remains, but the combination of Heartbeat lean cost discipline, supply chain rerouting, and pricing actions gives management multiple levers to defend margins.

Bear Case Valuation

In our bear case, if revenue growth stalls at 2%, margins remain flat at 15.3%, and the multiple compresses to 14x, GEHC trades at approximately $65-70 per share, representing 15-20% downside from current levels. Liquidation value (book value) of $10.6 billion in shareholder equity, or approximately $23 per share, provides a distant but real floor. The probability of a permanent capital loss from current levels is low given GEHC’s market leadership, recurring revenue base, and free cash flow generation.

SCENARIO ANALYSIS & IRR FRAMEWORK

Our $200 long-term target sits within the base-to-bull case range and delivers a 20.11% annualized IRR over 5 years. The probability-weighted expected value of approximately $183 per share implies that even accounting for downside scenarios, the expected 5-year return is highly attractive at roughly 18% annualized. The thing worth emphasizing is that the base case alone—which requires no heroic assumptions, just continued execution of strategies already underway—delivers a near-20% IRR. The bear case, which requires multiple simultaneous thesis violations (margin stagnation, innovation failure, and multiple compression), still produces a positive return from current entry levels. The asymmetry here is lopsided in our favor: moderate downside in failure, outsized upside in success.

The return is roughly evenly split between earnings compounding and multiple re-rating, which is the kind of dual-engine setup we look for in high-conviction positions. Pure earnings growth stories are vulnerable to multiple compression; pure re-rating stories are vulnerable to earnings disappointment. GEHC offers both simultaneously, which provides redundancy—even if one engine underperforms, the other can still deliver a strong return. Consider: if the multiple stays at 16x but EPS reaches $9.00, the stock trades at $144 (80% return). If EPS only reaches $7.00 but the multiple re-rates to 22x, the stock trades at $154 (93% return). You need both to fail for the investment to disappoint, and you need both to succeed to reach our $200 target—which is what we consider the most probable outcome.

MARKET MISPRICING THESIS & VARIANT PERCEPTION

What Is the Market Missing?

The market is pricing GEHC as a low-growth, mature medtech business trapped in the GE conglomerate legacy. The P/E of 16x implies minimal earnings growth. We think this narrative is wrong, and here is why:

1. The GE stigma is fading but not yet fully priced out. Three years post-spinoff, GEHC has established its own identity, yet the stock still trades at a massive discount to peers. As the company delivers 2-3 more years of consistent execution, the conglomerate discount will evaporate.

2. Tariff headwinds are masking underlying earnings power. Adjusting for the $0.43 tariff EPS impact in FY2025, earnings would have grown 12%. The Street is modeling tariff persistence, but GEHC is actively mitigating and management expects lower impact in 2026.

3. The innovation cycle is being under-credited. A 55% three-year vitality rate, photon-counting CT, Flyrcado, Freelium, and AI platforms represent the strongest product cycle in GEHC’s history. New products drive mix-up, higher margins, and revenue acceleration.

4. China conservatism creates a free embedded call option. Management is guiding for a China decline in 2026 despite improving KPIs (better VBP win rates, improving imaging funnel). If China stabilizes or recovers, it is pure upside not in the stock price.

5. The business model transformation is being valued at zero. The market is valuing GEHC as a cyclical equipment manufacturer, yet the company is systematically shifting its revenue mix from lumpy hardware sales toward sticky, high-margin recurring revenue: Intelerad adds cloud SaaS with 30%+ EBITDA margins, Flyrcado is a consumable diagnostics franchise with razor-and-blade economics, and CareIntellect/Genesis are building an AI software platform with network effects. At current multiples, you are paying for the legacy equipment business and getting the entire recurring revenue transformation for free. As this mix shift becomes visible in reported numbers, the market will be forced to re-rate the multiple.

Variant Perception Framework

If consensus believes GEHC is a 5-7% EPS grower deserving a 16x multiple, and reality reveals a 13-18% EPS compounder transitioning toward a recurring-revenue model as tariffs fade, innovation scales, and margins expand, then $80 per share is simply the wrong price. The near-term delta delivers $110. The compounding delta—sustained over 5 years as the market slowly reclassifies this business—delivers $200. That gap between the consensus narrative and the emerging reality is where the alpha lives, and patience is how you capture it.

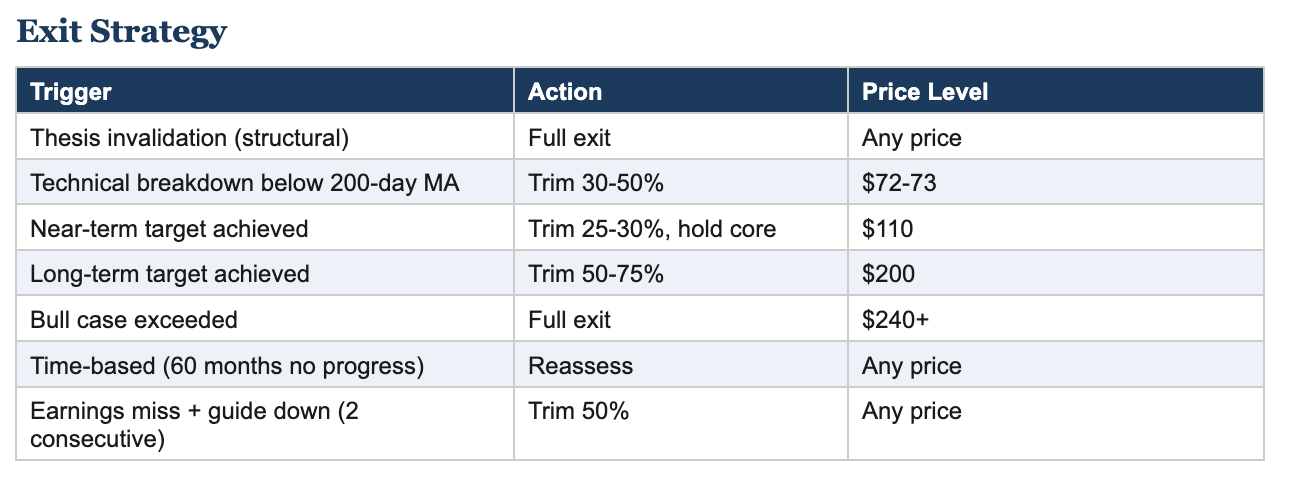

POSITION SIZING & EXIT STRATEGY

Position Sizing Framework

For Guardian Research portfolio context, GEHC represents our highest conviction idea. Given the asymmetric risk/reward profile (3.8:1 upside/downside), we note a 6-10% portfolio weighting as a sweet spot for active investors. For more conservative allocations, a 3-5% weighting provides meaningful exposure with manageable risk. Position sizing should be adjusted for individual risk tolerance, portfolio concentration limits, and the 1.23 beta.

The exit strategy is designed around the dual-target framework. At $110, the near-term thesis is validated, but the long-term compounding story is just getting started—trimming a quarter of the position locks in profits while maintaining substantial exposure to the 5-year return. At $200, the majority of the long-term thesis is realized and risk/reward becomes more balanced, warranting a larger trim. Only a structural thesis invalidation—such as a fundamental deterioration in competitive position, a failed Intelerad integration, or a sustained reversal in the recurring revenue trajectory—warrants a full exit at any price. Patience is the critical ingredient: premature selling in a compounding story is the most common way investors leave money on the table.

HISTORICAL ANALOG COMPARISON

The most relevant historical analog for GEHC is the corporate spinoff value creation pattern observed across hundreds of separations. Academic research consistently shows that spinoffs outperform the market by 10-20% in the 2-3 years following separation. The value creation typically follows a three-phase pattern: Phase 1 (Year 1) involves establishing independent operations, overhang selling by index funds, and initial investor re-rating. Phase 2 (Years 2-3) involves operational improvements, incentive alignment, and earnings acceleration. Phase 3 (Years 3-5) involves full value recognition as the company establishes a track record.

GEHC is at the transition from Phase 2 to Phase 3. The GE Vernova analog is particularly instructive: GEV’s stock languished in its first months post-spinoff before exploding higher as the AI-energy narrative took hold. GEHC’s narrative catalyst—the innovation renaissance and margin expansion story—may take 12-18 months to fully embed in consensus models, but the fundamental building blocks are already in place.

CONCLUSION: THE ALPHA OPPORTUNITY

GE HealthCare Technologies is a franchise-quality medtech business with a $20.6 billion revenue base, a record $21.8 billion backlog, the strongest innovation pipeline in its 130-year history, and an experienced management team executing a clear value creation strategy. The stock trades at approximately $80 per share, or 16x forward earnings—a 40%+ discount to the medtech peer group.

The market is anchored to a narrative of low growth and GE conglomerate baggage. We believe the reality is different: GEHC is entering a multi-year earnings compounding cycle driven by innovation scale-up (Flyrcado, photon-counting CT, AI platforms), margin expansion (Heartbeat lean, tariff mitigation, SG&A leverage, recurring revenue mix shift), capital return (buybacks, Intelerad accretion), and potential China recovery. We model a clear path to $5.90-6.10 in EPS by 2027 supporting our $110 near-term target, and $8.50-9.50 in EPS by 2030 supporting our $200 long-term target at a still-discounted 22-24x multiple. The 20.11% annualized IRR over 5 years is driven by the rare combination of double-digit earnings compounding and structural multiple re-rating—a dual engine that provides redundancy even if one pillar underperforms.

This is our highest conviction idea because the variant perception is clear, the catalysts are identifiable and time-bounded, the downside is limited by the franchise’s defensive characteristics, and the upside is substantial. The market is pricing a hardware dinosaur. What we see is a company in the early innings of a transformation into a recurring-revenue healthcare technology platform. The near-term setup is attractive—if Q1 2026 margins confirm the expansion trajectory, the stock reprices quickly toward $110 as institutional models catch up. But the real wealth creation happens over the next five years as the earnings compounding story plays out. Patience is required, but it is well rewarded at these levels. We think GEHC is the most overlooked compounder in medtech today.

GEHC to $200

GUARDIAN RESEARCH

DISCLAIMER: This report is for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.