5x From Here: $ANGX

The non-woke Netflix at 1.6x ARR while Spotify trades at 6.5x. A director just bought $1mm in the open market.

Three dollars and change for the only audience-curated film studio at scale, with 2.22mm paying members, $365mm in annualized recurring revenue, and a Q1 2026 print that turned adjusted EBITDA positive at $4mm. Operating cash flow also turned positive at $1.9mm. The market cap sits at $585mm. The Guild alone trades at roughly 1.6x ARR. Spotify trades at 4.2x. Netflix at 8x.

What the bears point to. Two dilutive equity raises in three months, the most recent in April 2026 at $2.10. A 2025 net loss of $170mm. Three pending all-stock acquisitions priced at $6.13, almost double current. SPAC stink. Lockup expirations ahead. Generalist managers won’t touch faith-adjacent content brands.

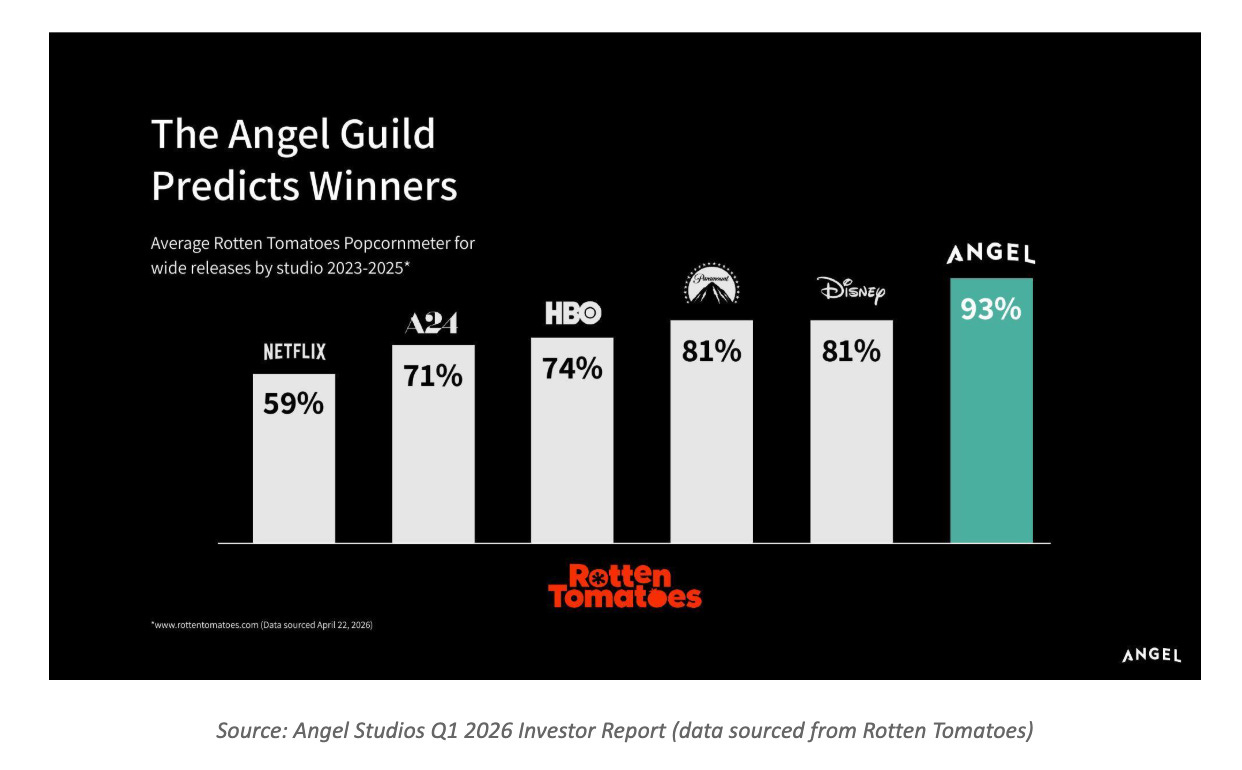

What gets ignored. Guild revenue went from 1% of mix in 2023 to 72% of Q1 2026 revenue. Membership doubled YoY from 1.08mm to 2.22mm. ARPU is $13.69 per month and rising. Adjusted EBITDA turned positive a full quarter ahead of any reasonable expectation. Apple Partner program adds $300k/month of incremental pure margin. Angel’s wide-release Rotten Tomatoes Popcornmeter average is 93% versus Netflix at 59%, A24 at 71%, HBO at 74%, Paramount at 81%, and Disney at 81%. And a board director, Steven Sarowitz, just put $982k of his own cash on the tape at $3.06.

Sarowitz founded Paylocity in 1997 and took it public in 2014. He sits on the board. He has access to internal financials and pipeline data the public doesn’t. He’s been involved with the company since May 2025 through a $5mm convertible note at a $6.13 strike. He kept buying when the equity sold off. That signal carries weight NO sell-side initiation or upgrade can match.

The thesis runs simple. Public markets vaporized the SPAC discount and threw out the operating business with the bathwater. Most de-SPACs earned that obloquy. Angel didn’t.

The Insider Buy: A $1mm Open-Market Vote

On May 5, 2026, Director Steven I. Sarowitz purchased 321,544 shares of ANGX Class A at an average price of $3.0558. Total outlay: $982,355. Post-transaction direct holdings: 326,840 shares. Form 4 coded P. Open-market purchase. Not a derivative settle, not a grant, not a 10b5-1 trickle. He walked onto the tape and bought.

Sarowitz’s involvement with Angel runs deeper than this one buy. He founded Paylocity (NASDAQ: PCTY) in 1997, took it public in 2014, and serves as Chairman. Forbes pegs his net worth around $2bn. In May 2025, the controlling entity behind a $5mm subordinated convertible note (struck at $6.13 per share) was him. He joined the ANGX board in September 2025 at the SPAC closing. He participated in the company through three rounds of financing before the public listing, then bought aggressively in the open market when the stock got punished. The pattern doesn’t look anything like a passive director collecting board fees. It reads as an operator with conviction adding size after the equity got punished.

Form 4 buys at depressed prices by directors with operating experience and disclosed deep pockets are about as clean a signal as the disclosure regime produces. Sarowitz chose to add at $3.06. That signal beats any sell-side initiation by a country mile.

The Non-Woke Netflix Angle

The pitch in a sentence: ANGX is the streaming platform for the audience Hollywood deliberately walked away from.

Pew has tracked American trust in legacy media for fifteen years. The number has only ever fallen. Hollywood produces for a coastal audience that represents perhaps 25-30% of the domestic consumer base on a charitable read. The remaining 70% has been asking for product they don’t have to apologize for at the dinner table. Sound of Freedom did $250mm at the global box office on a $14.5mm budget. The 2025 slate alone generated $211.9mm in domestic box office across 8 releases, with David ($83.9mm) and The King of Kings ($83.2mm) each landing in the top 10 animated releases of the year. Angel was the #10 domestic distributor in 2025 per TheNumbers.com.

The Rotten Tomatoes audience scores tell a story management could put on a billboard.

A 34-point spread against Netflix. A 12-point spread against Disney. The Popcornmeter is the open scoring system the entire industry uses, surveying viewers across the universe of moviegoers rather than a single platform’s subscribers. The Guild selects content that audiences actually like at a hit rate the major studios cannot match. The Guild’s votes happen upstream of the greenlight decision.

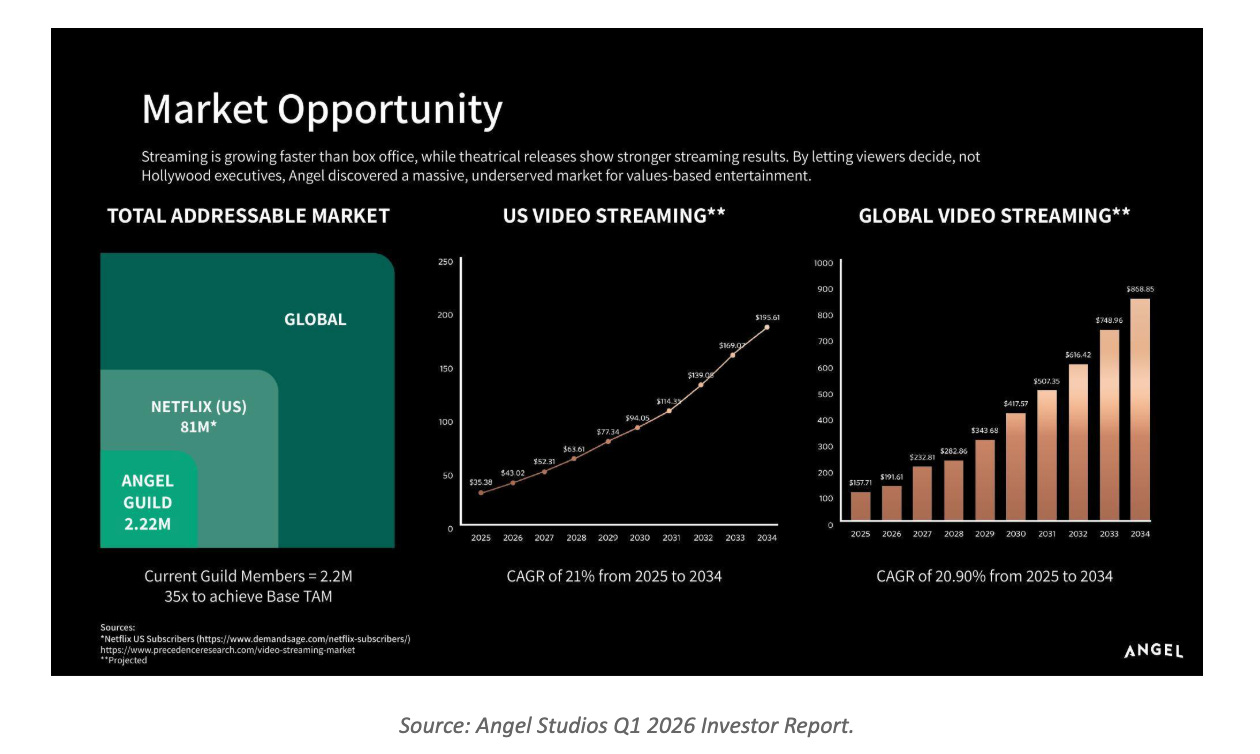

Calling this a faith-based niche misses the point. Faith-based was the wedge. The real addressable market is general audiences hungry for clean, family-resilient, value-positive storytelling with actual stakes. Netflix has 81mm domestic households. Angel has 2.22mm paying Guild members. Capture even 10% of the cultural audience that explicitly avoids Hollywood output, and Angel becomes a 7-10mm subscriber business at $20+ ARPU, doing $1.5bn to $2bn in revenue at 65%+ subscription mix on a fixed cost base that doesn’t scale linearly.

Netflix spent $16.2bn on content in 2024 and projects $18bn in 2025, and still struggles with audience fatigue on prestige slates. Angel has paid out a cumulative $254.6mm to filmmakers, with the Guild itself deciding which projects get greenlit. Production risk stays off Angel’s balance sheet. The company splits 50% of Guild streaming profits with filmmakers and 67% of all distribution profits, which aligns directors and producers around upside while building a content engine that doesn’t demand studio capex. The model is remunerative for filmmakers in a way the traditional studio system cannot match.

Forget the Netflix framing. The bet is that Angel ends up the highest-margin niche streamer in the country.

How Angel Got Its Name: From the Angels Who Funded It

In 2013, Neal Harmon and his brothers (Daniel, Jeffrey, Jordan) plus cousin Benton Crane founded VidAngel, a service that let parents filter explicit content from streamed films. Disney, Warner Bros., Fox, and Lucasfilm sued in 2016 for copyright infringement. The legal battle drove VidAngel into Chapter 11. The Harmons settled in 2020 for $9.9mm against an initial $62.4mm judgment, sold off the filtering business, and rebranded the parent entity as Angel Studios in 2021. The Disney settlement was fully repaid by September 30, 2025.

No venture round saved them. The bridge through bankruptcy came from 18,000-plus individuals writing small checks via Regulation A+ and Regulation Crowdfunding offerings, plus follow-on Reg A offerings tied to specific projects. The Chosen alone raised $11mm in equity crowdfunding for its first season. Tuttle Twins raised $4.6mm. The Wingfeather Saga raised $5mm. Through the VAS Portal funding platform, Angel has now facilitated investment in dozens of individual films.

Those small investors got equity in the films and in the company. They were the angels. Neal Harmon named the studio after them. The Guild is what those angels became, productized into a recurring subscription with voting rights, free theatrical tickets, and a felt sense of ownership over the greenlight decision. The lineage runs unbroken. The economic engine today is that crowdfunding base wearing a subscription jersey.

This matters because it tells you who Angel’s audience actually is. Angel’s audience holds something closer to equity than to a subscription. Stakeholders, in plain terms. The retention math that follows runs downstream of that distinction.

The Guild: The Recurring Revenue Engine

This is the section that should make a generalist analyst sit up.

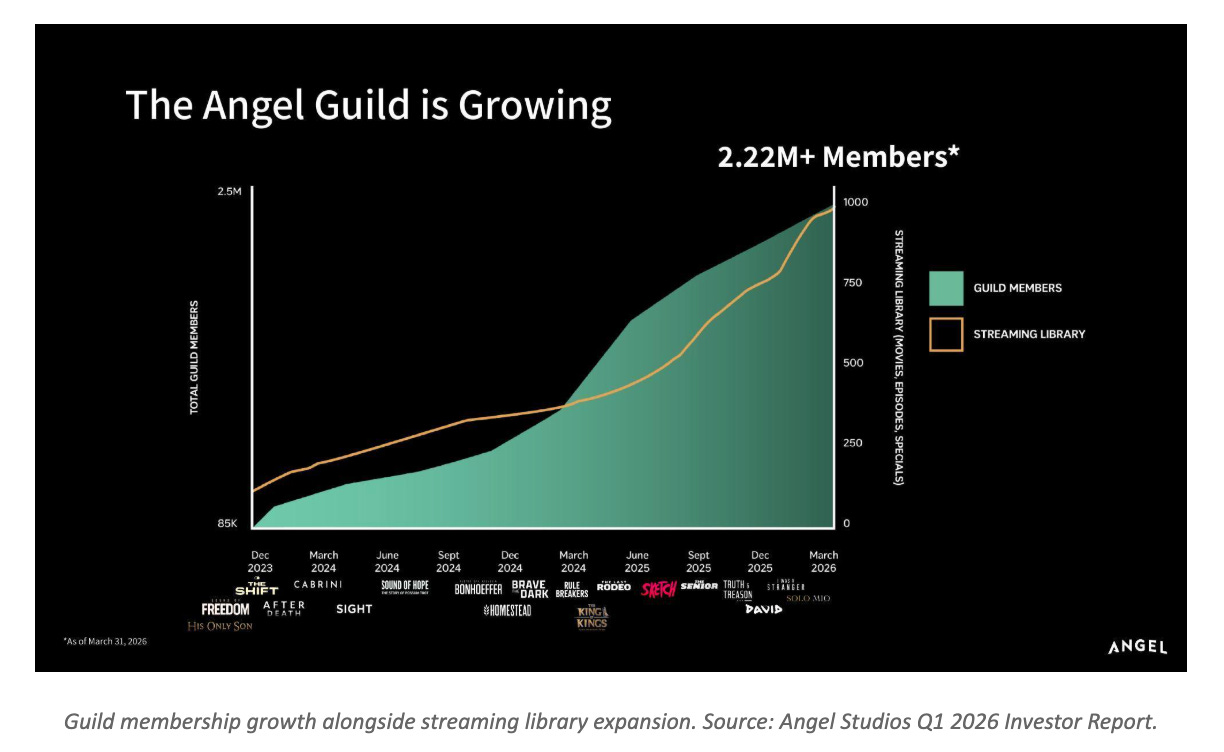

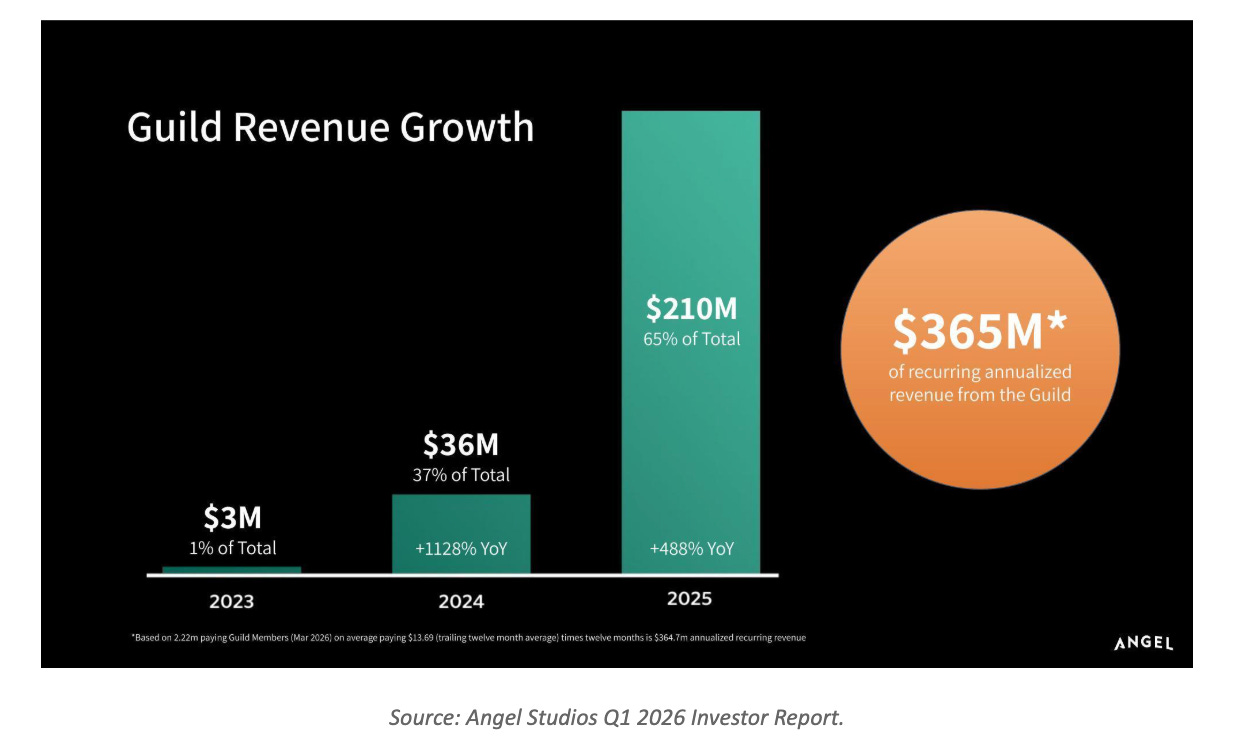

Guild trajectory

Dec 2023: ~85k members, Guild revenue $3mm (1% of total)

Dec 2024: ~700k members, Guild revenue $36mm (37% of total, +1,128% YoY)

Dec 2025: 2.0mm members, Guild revenue $210mm (65% of total, +488% YoY)

Mar 2026: 2.22mm members, $365mm annualized recurring revenue (72% of Q1 2026 revenue)

Guild revenue grew at triple-digit rates for two consecutive years. Q1 2026 added 220k net new members, 11% sequential, 106% trailing twelve-month. The $365mm ARR figure is implied run-rate from 2.22mm members times $13.69 trailing twelve-month ARPU times twelve months. That math falls right out of the filings.

Pricing tiers

Basic with Ads

Basic: $8.99/month or $99.99/year

Premium: $14.99/month or $149/year, including two complimentary theatrical tickets per release and merchandise discounts

Angel sits at the bottom of the U.S. streaming pricing band. Most major services charge $13 to $30 per month for premium ad-free tiers. Angel Premium at $14.99 lands below Hulu no-ads ($18.99), Disney+ no-ads ($18.99), HBO Max no-ads ($18.49), and Netflix Standard no-ads ($17.99). The hook is curation and values. That’s pricing power legacy SVOD competing on scale and library size doesn’t get to enjoy.

ARPU

$13.69 per month trailing twelve months. That is $164 in annual revenue per active member. Mix shift toward Premium and annual lifts this materially. Premium pricing alone pushes the company toward $20+ monthly ARPU at scale if mix lands where management implies.

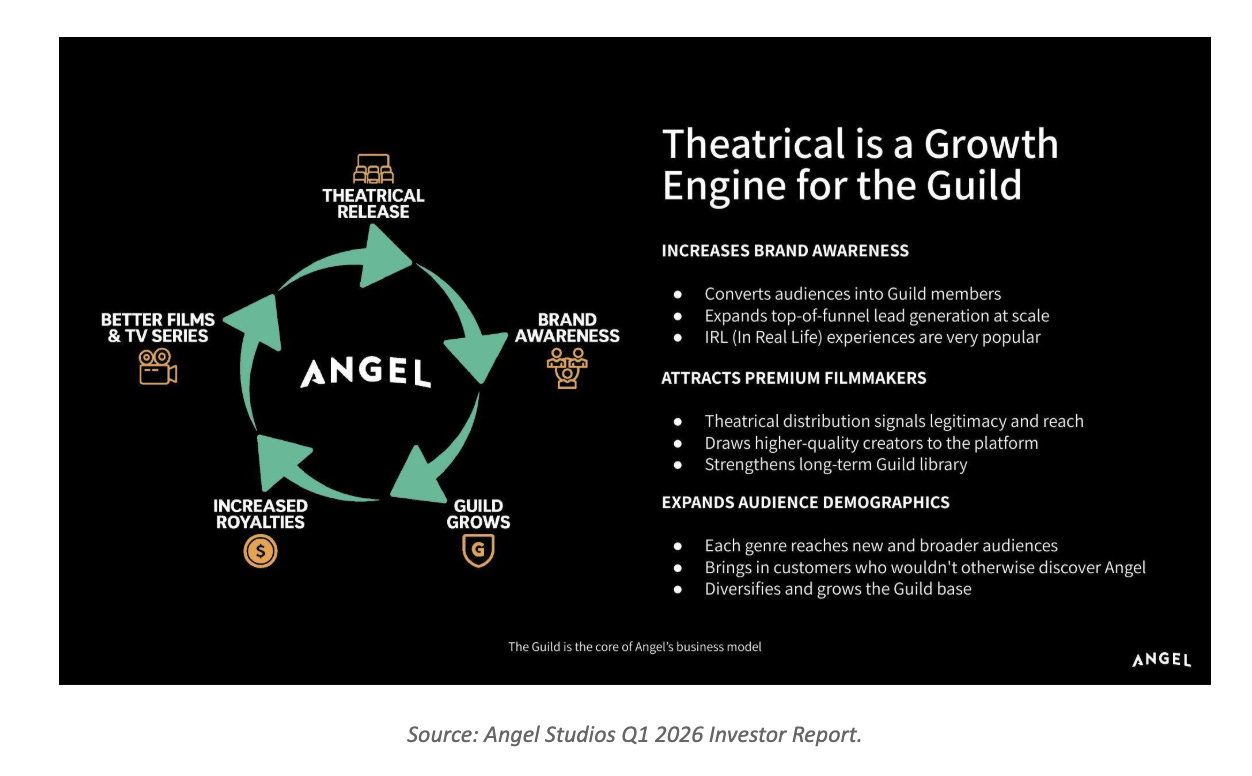

The flywheel (management’s framing, validated by the data)

Theatrical release drives brand awareness. Brand awareness drives Guild signups. Guild signups generate royalties for filmmakers. Royalties attract better filmmakers. Better films and TV series fuel the next theatrical release. The cycle compounds.

Most streamers spend on content and hope an audience finds it. Angel runs the loop backwards. The audience commits and votes before anything gets greenlit, and content gets made off the back of those votes. Production risk drops because the audience pre-selected what they wanted. The 93% Rotten Tomatoes audience score is the downstream proof the loop works.

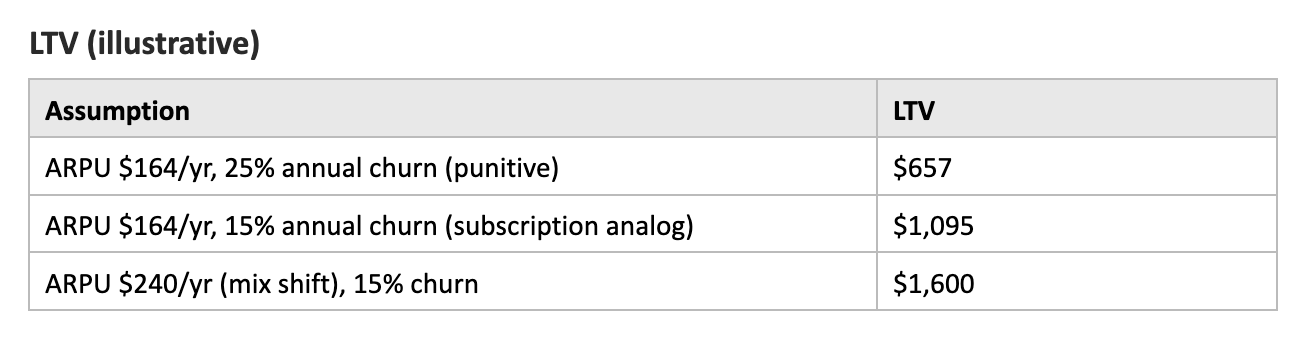

LTV/CAC and Retention

The numbers in the 10-Q make the unit economics explicit. ARPU of $13.69 is monthly, not annual. That puts annual ARPU per active member at $164.28, and the LTV math falls out cleanly from there.

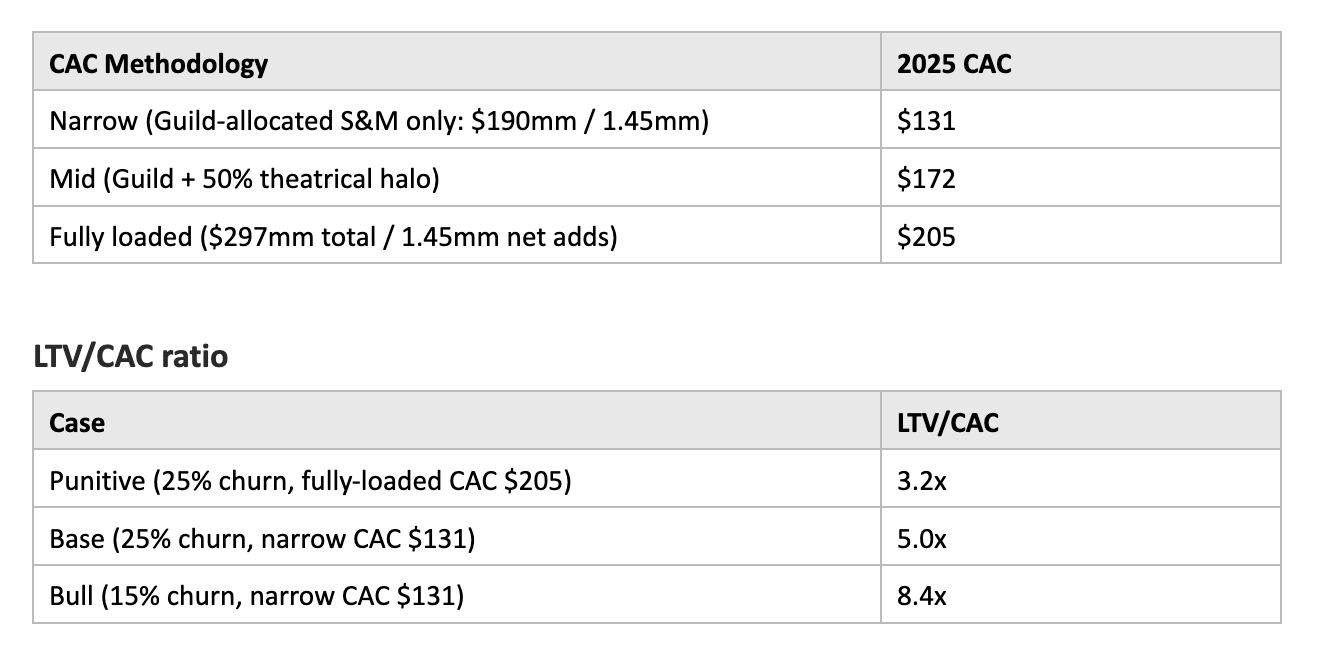

CAC

2025 sales and marketing spend was $297mm. Net Guild adds in 2025 were approximately 1.45mm members (from roughly 550k at year-end 2024 to 2.0mm at year-end 2025).

The Q1 2026 S&M breakdown gives the cleanest read on what portion drives Guild acquisition directly:

Q1 2026 Angel Guild S&M: $36mm

Q1 2026 Theatrical S&M: $17mm

Q1 2026 Other S&M: $3.5mm

Total: $56.6mm

Roughly 64% of S&M is allocated to Guild promotion directly. Theatrical S&M is positioned by management as a Guild acquisition tool with secondary box office monetization. Applied to 2025:

Anything north of 3x is healthy. Above 4x with payback under twelve months is best-in-class subscription media. ANGX is plausibly there now. Premium mix and annual conversion drive the ratio higher from here. Payback period at fully-loaded CAC and current ARPU comes in under 16 months. At the narrow case, payback drops below 10 months.

The operating leverage tell. Q1 2026 turned adjusted EBITDA positive at $4mm on $115mm revenue. The fixed cost base doesn’t scale with marginal subscriber. Each new Guild member sits closer to pure contribution than the last. Q1 2026 operating cash flow also turned positive at $1.9mm. The inflection is showing up in the actual financial statements today rather than as a forward-looking projection.

Bitcoin Treasury

Angel holds 303.1 bitcoin as of March 31, 2026, carrying value $20.7mm, cost basis $19.6mm. Management has articulated a treasury strategy to potentially expand holdings, collateralize borrowings, and periodically monetize for working capital. In October 2024, Off the Chain (a bitcoin asset management firm) bought $10mm of Class A at $5.66, payable in bitcoin, as part of formalizing the strategy.

This is a smaller position than the Saylor playbook but the optionality is real. At 1.79 BTC per million shares outstanding, the position is non-trivial relative to the small float. Q1 2026 mark-to-market loss on the digital assets was $5.8mm, which drove most of the gap between the $4mm positive adjusted EBITDA and the $13.8mm net loss. Sensible people can argue about whether a media company should hold any bitcoin at all. At 303 coins, though, the position is too small to swing the cash story in either direction.

Three Roll-Up Acquisitions at $6.13 (The Quiet Signal)

On November 14, 2025, Angel signed three all-stock merger agreements at a $6.13 per share valuation:

Black Autumn / Homestead (film and TV series rights)

Toothy Cow Productions / The Wingfeather Saga (animated series)

Tuttle Twins Show, LLC (libertarian-themed children’s series)

These are content IP roll-ups. Angel is consolidating three of its highest-performing franchises into the corporate parent by issuing stock at $6.13. Today’s stock price is $3.14. Management is paying nearly 2x current market for IP it could buy back for half by simply waiting.

Two interpretations exist. Either management is materially overpaying for content rights, or management believes the equity is materially undervalued at $3.14 and is willing to issue at a valuation that reflects something closer to fair value. The $6.13 number is consistent with the Sarowitz convertible note strike ($6.13), the prior September 2025 Reg A pricing ($8.23), and the Off the Chain transaction ($5.66 a year and a half earlier). Multiple data points say management has been pricing the equity in the $5 to $8 zone for the last 18 months.

The April 2026 underwritten offering at $2.10 broke the pattern. That raise (16.4mm shares for $34.5mm) was opportunistic balance sheet repair, not a fair-value signal. $6.13 is the marker management keeps printing on value-creation transactions. $2.10 was liquidity desperation. Intrinsic sits closer to the former.

SPAC Structure

ANGX came into public-market existence on September 10, 2025, when Angel Studios Legacy merged with Southport Acquisition Corporation, a blank-check SPAC originally targeting financial software. Southport was led by CEO Jeb Spencer (co-founder of TVC Capital) and Chairman Jared Stone (co-founder of Northgate Capital). The combined enterprise was valued at $1.6bn at deal close. The accounting was a reverse recapitalization with Angel Legacy as the accounting acquirer.

The balance sheet is funded. Cash at March 31, 2026 was $38.9mm, plus the $34.5mm April 2026 raise nets to roughly $73mm pro forma, minus the $38.5mm P&A loan repaid in April. Effective post-April cash sits in the $35mm range against $102mm of notes payable. The $100mm term loan facility (13.5% interest, $60mm drawn so far) has another $40mm available subject to ARR milestones. Bitcoin holdings of $20mm offer collateral optionality. 2026 adjusted EBITDA loss guidance caps at $25mm with Q1 already positive. Cash burn risk is largely off the table, though the leverage at 13.5% interest is non-trivial and worth monitoring.

Management and Board

Executives

Neal Harmon, CEO and Chairman. Co-founder. Master’s in Instructional Psychology and Technology from BYU. Built and exited Orabrush before VidAngel. The operator and chief evangelist. 48 years old.

Jordan Harmon, President. Day-to-day operations and theatrical strategy. 2026 base salary $430k plus 169k RSUs and 71k PSUs under the 2025 LTIP. 35 years old.

Jeffrey Harmon, Chief Content Officer. Co-founder of Harmon Brothers, the marketing agency behind Squatty Potty and other viral DTC campaigns. 43 years old.

Elizabeth Ellis, COO. 49 years old.

Scott Klossner, CFO. 35-year public company veteran. Previously CFO of Field Nation. Before that, CFO of Mercato Partners Acquisition Corp (SPAC merged with Nuvini, where he remains a director). Before that, CFO of Kount (sold to Equifax for $640mm in 2021). Before that, CFO of Backcountry.com (sold to Liberty Media in 2007). 2026 base salary $415k plus 113.5k RSUs and 58k PSUs. He gets hired by growth companies and gets them to exits.

Glen Nickle, Chief Legal Officer and Secretary.

Board

Neal Harmon (Chairman, CEO)

Paul Ahlstrom (Director, longstanding from Alta Ventures era)

Katie Liljenquist (Director)

Mina Nguyen (Director)

Steve Sarowitz (Director, Paylocity founder, recent $982k open-market buyer)

Robert C. Gay (Director, Harvard PhD Business Economics, Phi Beta Kappa)

Benton Crane (Director, co-founder, joined board October 22, 2025)

The Harmons run product, culture, and slate. Klossner runs the public company plumbing. Sarowitz and Gay add board ballast and operating wisdom. The shape of the team is right for the moment.

Headcount: 290 full-time plus 21 part-time as of December 31, 2025. Per the IR deck, 80+ are in product and engineering. Management cites 10x productivity gains in select functions from AI tools and 12% lift in average watch time per A/B test on AI-driven discovery. Most of the 300+ team is now building with AI.

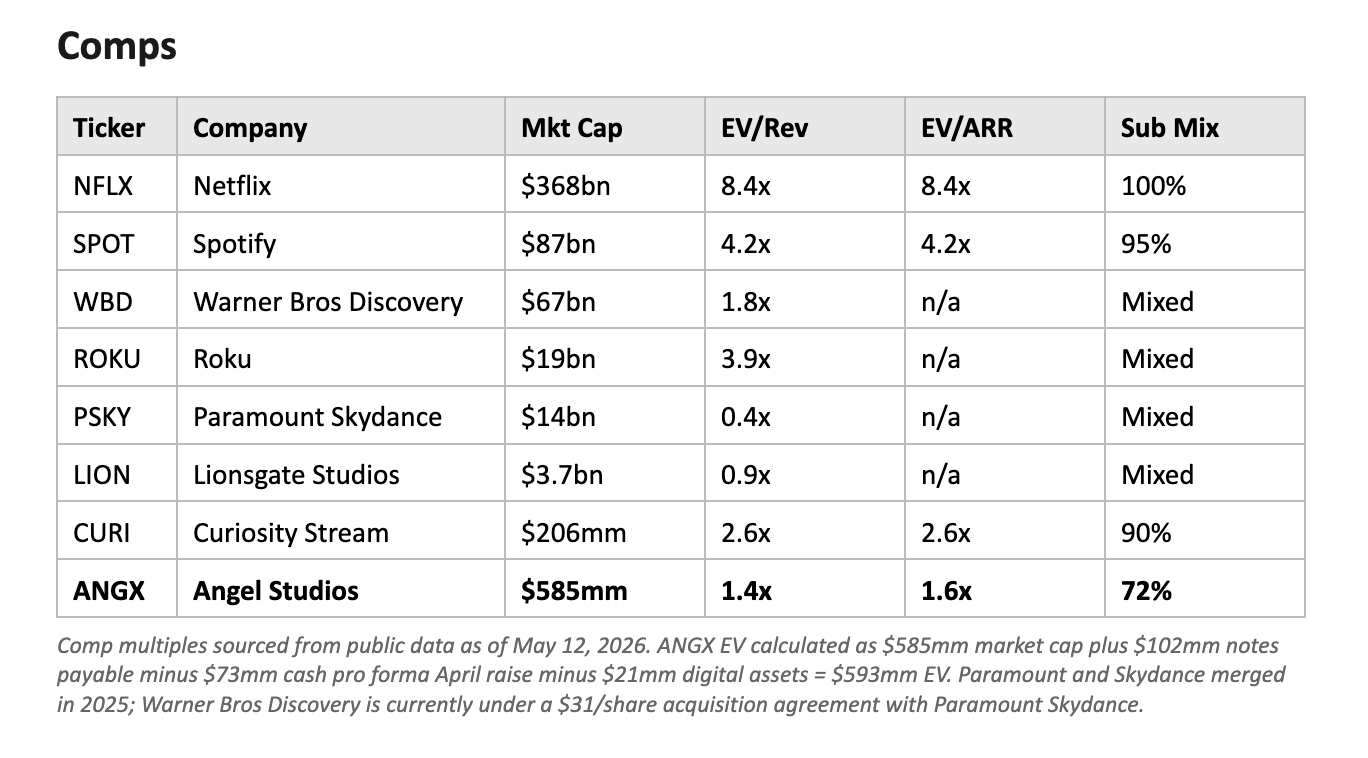

ANGX trades at 1.6x ARR on Q1 2026 run-rate. Spotify trades at 4.2x today, down from 6.5x in 2024 on softer guidance. Roku at 3.9x EV/Rev offers another digitally-native streaming reference point. Curiosity Stream, the smallest comparable niche streamer, trades at 2.6x. ANGX sits below every meaningful comparable in the set.

Apply a deeply discounted 2.5x multiple to $365mm ARR. The implied equity value is $913mm, or roughly $4.90 per fully diluted share. Floor case.

Apply SPOT’s current 4.2x to forward ARR scaling to $600mm by end-2026 (realistic on current run-rate plus mix shift). The math gets to $2.52bn equity, or $13.50 per fully diluted share. Apply pre-compression SPOT multiples or a small premium for differentiated content moat, and the math runs to $16 to $18 territory. The PT sits in that range.

Macro and Thematic

Cultural realignment. Hollywood spent the last decade alienating somewhere between 30% and 60% of the U.S. audience depending on how you measure. Economic consequences now show in box office data, theme park attendance, Disney+ churn, and slow grinding legacy media consolidation. Paramount Skydance is acquiring Warner Bros Discovery at $31 per share. WBD took a $2.9bn charge in Q1 on the Netflix termination fee tied to that deal. The legacy bundle is being unwound in public. That audience didn’t disappear. They stopped showing up for product that insulted them. Angel orients toward them explicitly, without the apology routine. The 93% Rotten Tomatoes average versus Netflix at 59% quantifies what cultural commentators have argued for years. The tailwind is real. It’s not in the multiple.

Cord-cutting still has runway. Per IBISWorld, the U.S. video streaming industry has compounded at 6.9% annually over the past five years to reach $102.8bn. Eighty-three percent of U.S. adults now watch programming on streaming services. Streaming has become the default mode of television viewing, but the structural shift from cable and satellite is nowhere near finished. Every cord cut is a household reshuffling its streaming wallet.

Subscription fatigue and the ad-supported pivot. Big platforms are in price-increase mode because domestic subscriber growth has flatlined. Netflix is rolling ad tiers and cracking down on password sharing. Spotify guided down on margins and got punished. Subscription fatigue is real. Ad-supported tiers have emerged as the most profitable model in streaming, with ARPU on the ad-supported side expected to surpass ad-free in coming years. Angel’s Basic with Ads tier sits in exactly that lane. Premium subscribers churn less. Ad-supported is the on-ramp that pulls families into the platform at a lower commitment level. Angel’s model is shaped for where streaming is heading.

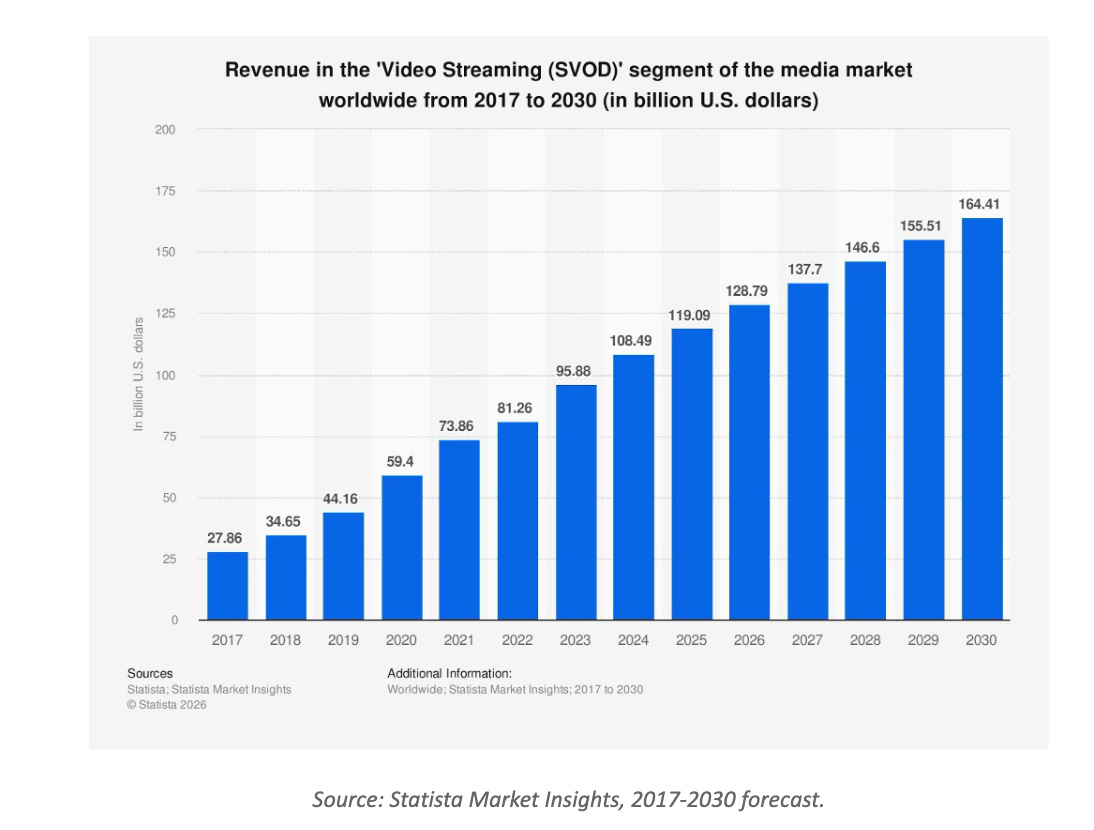

Global SVOD TAM keeps compounding. Worldwide SVOD revenue is forecast to grow from $128.8bn in 2026 to $164.4bn by 2030. The pie is expanding even as legacy media consolidates.

Original content as moat. Industry research consistently flags original content as the durable differentiator for streaming platforms. Licensed catalogs come and go on volatile contract cycles. Original IP builds brand. The 18-34 demographic, streaming’s largest segment, leans into niche, culturally specific content over generic studio output. Angel’s Guild-selected slate maps directly onto that preference. The Guild votes before greenlight. The platform owns the IP outright via three pending acquisitions at $6.13. The flywheel reinforces the moat.

AI cost curve. Angel disclosed 10x productivity gains in certain functions from AI adoption, plus a 12% increase in average watch time per A/B test on AI-driven discovery. Content production and distribution costs are falling fast for digitally native operators. Angel was born one. Legacy studios are still bolting modern tech onto analog foundations, and the gap widens with every model generation. The company runs an 80+ person engineering org building proprietary platform technology, integrated ticketing, and first-party data systems that trace conversions back to specific ads. Industry research now flags AI integration as a primary success factor for modern streaming businesses, both for personalized recommendations and for predictive analytics that evaluate likely show performance before greenlight. Angel runs that loop natively.

Production tax incentives. State-level production tax credits in California, New York, Illinois, New Jersey, and Wisconsin have been sharply expanded to explicitly cover streaming projects. The proposed federal CREATE Act would allow producers to deduct 100% of qualified production costs in the year incurred. Angel’s filmmaker partners benefit directly when projects qualify. The economics of an Angel-distributed independent film improve at the margin from every credit captured.

Theatrical as marketing line item. Management has been explicit that theatrical releases run as loss-leaders for Guild acquisition. Sounds like an excuse until you do the conversion math. A $20mm to $30mm domestic box office release brings 100k to 300k new Guild signups, which at $164 annual ARPU represents $16mm to $49mm in year-one revenue. Theatrical pays for itself through Guild conversion before licensing and merch revenue arrive. The 2025 slate generated $211.9mm in domestic box office across 8 releases, and Guild membership grew from roughly 550k to 2.0mm over the same period. Solo Mio crossed $25mm domestic in Q1 2026 alone. The conversion is happening.

Demographic tailwind. Family formation rates have been climbing in the demographic Angel serves. Larger household sizes mean higher per-account ARPU on family plans and more aggregate demand for content the whole household can watch. Cultural niches rarely have demographic wind at their back. This one does.

Recent Catalysts and Analyst Coverage

Tape action over the last three weeks. In rough chronological order:

April 30, 2026: Q1 2026 earnings beat. Revenue $115.1mm versus $107mm consensus. EPS loss $0.08 versus $0.11 expected. Adjusted EBITDA flipped to positive $4mm from negative $28.7mm year-ago. Stock +15.4% the next day. Gross margin expanded to 62% from 59%. Selling and marketing expense fell from 107% of revenue in Q1 2025 to 49% of revenue in Q1 2026. That is operational leverage showing up in real numbers, not management talking points.

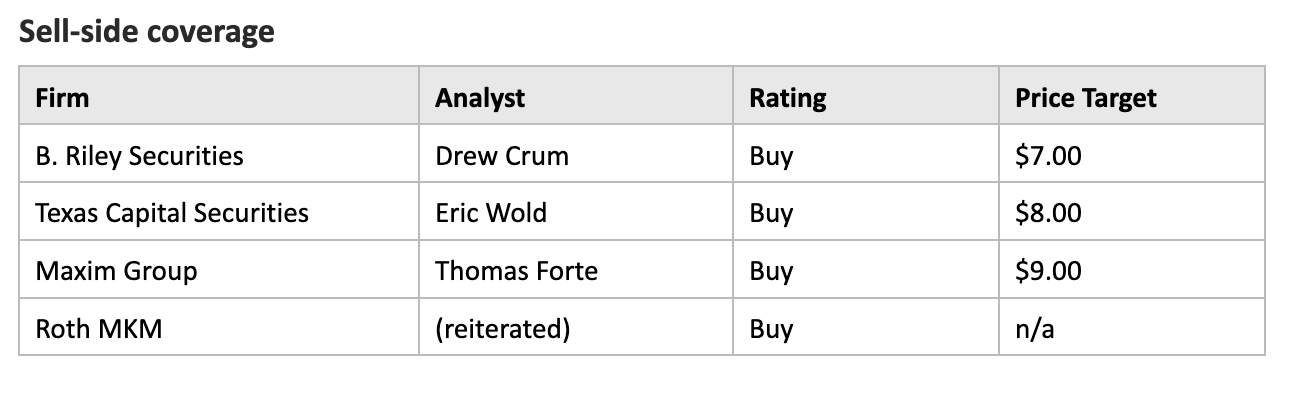

May 1, 2026: Roth MKM reiterates Buy. First post-earnings analyst confirmation.

May 1, 2026: Solo Mio crosses $25mm domestic box office. The Q1 2026 theatrical highlight. Continued evidence the slate is converting.

May 2, 2026: SOX 404 internal control risk flagged. Public disclosure of heightened internal control challenges as the company approaches accelerated filer status. Worth tracking. Material weakness disclosure would be a negative event.

May 5, 2026: Sarowitz buys $982k of common at $3.06. Form 4 P-coded open-market purchase. Detailed in the Insider Buy section above.

Six firms cover the name with a consensus rating of Outperform. Average analyst price target sits between $7.80 and $9.75 depending on the source. The Texas Capital target was raised from $6.50 to $8 after Q4 2025. My $16 PT sits roughly 2x consensus, which is consistent with thinking the multiple expansion isn’t yet priced in by mainstream sell-side.

Consensus revenue for FY2026 is $458.87mm (up from $412mm 90 days ago). FY2027 consensus revenue is $577.57mm. Q1 2026 came in $8mm above consensus. The pattern of upward revisions plus beat-and-raise quarters tends to attract incremental coverage. Mainstream small-cap funds and sector funds catch up after two or three of these in a row. Six firms today. Twelve in eighteen months is reasonable.

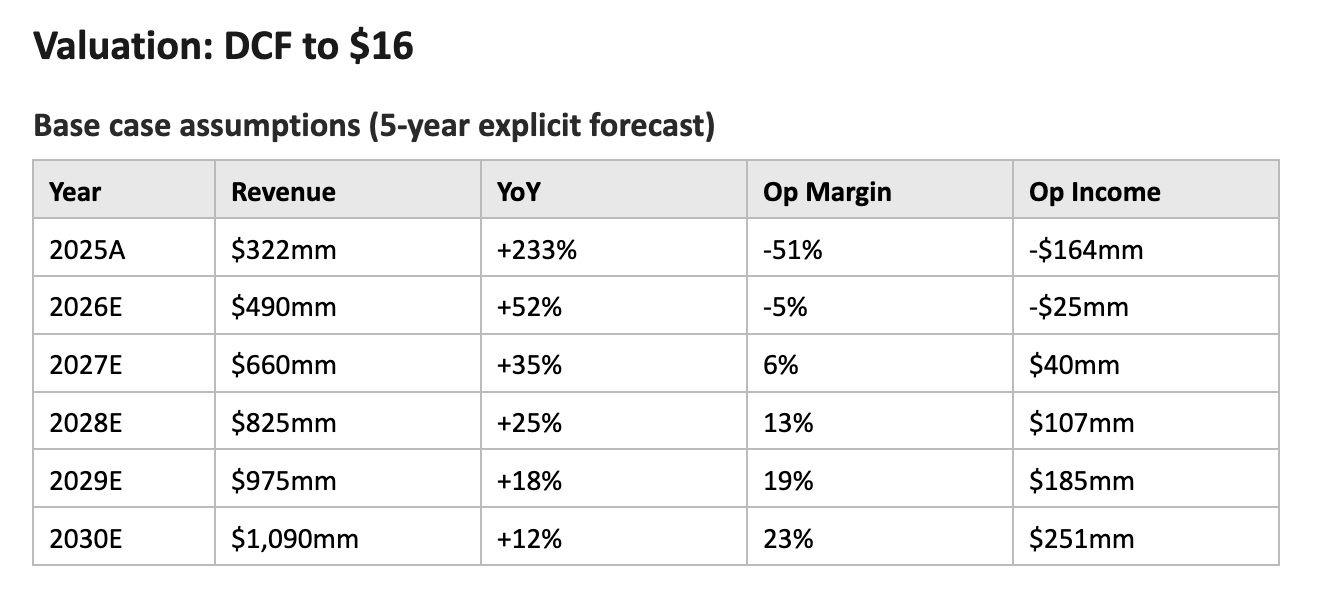

Guild ARPU expansion: $13.69/month to roughly $20/month by 2030 on mix shift to Premium and annual

Guild membership: 2.22mm today to 7-9mm by 2030

Terminal growth: 3%

WACC: 12% (size, beta, SMID equity risk premium)

Terminal value: ~$2.9bn

Discounted terminal plus cumulative DCF: ~$3.5bn equity value

Fully diluted shares: ~222mm currently, ~232mm post-acquisitions

Implied per share: ~$15 to $16

The DCF here is back-of-envelope. The full version belongs in the three-scenario template. $16 central case. $7 bear case (slower Guild growth, churn surprises, margin stays compressed). $24 bull case (Spotify-comparable multiple holds, ARPU expands, AI cost curve gets steeper).

Risks

Content miss cycle. A string of theatrical underperformers breaks the Guild conversion engine. The 2026 slate (I Was A Stranger, Solo Mio, Animal Farm, Young Washington, Zero A.D.) is unproven.

Churn surprises. Management hasn’t disclosed monthly churn explicitly. The lacuna is real. Materially worse-than-implied churn cracks the LTV math.

Pending acquisition dilution. Three all-stock deals at $6.13 add 8-15mm shares.

April 2026 raise dilution. 16.4mm shares at $2.10 was severely dilutive. Another raise at depressed prices would not be welcomed.

Term loan leverage. $60mm drawn at 13.5%, with up to $40mm more available subject to ARR triggers. Quarterly interest expense already $6mm.

Bitcoin volatility. 303 BTC is small but mark-to-market losses ($5.8mm in Q1 2026 alone) drag reported net loss.

Insider lockup expirations. Sponsor and founder lockup schedules roll on a defined calendar. Track carefully.

SPAC residual stink. Some institutionals won’t touch a former SPAC for two years post-de-SPAC. Suppresses multiple expansion.

Competition from incumbent streamers in faith-adjacent content. Less likely than headline risk suggests. Disney’s family slate is worth watching.

Going concern absent operating discipline. The 10-Q signals 12+ months of runway. Going concern is not currently flagged. Stays that way only if EBITDA stays positive and operating cash flow stays positive.

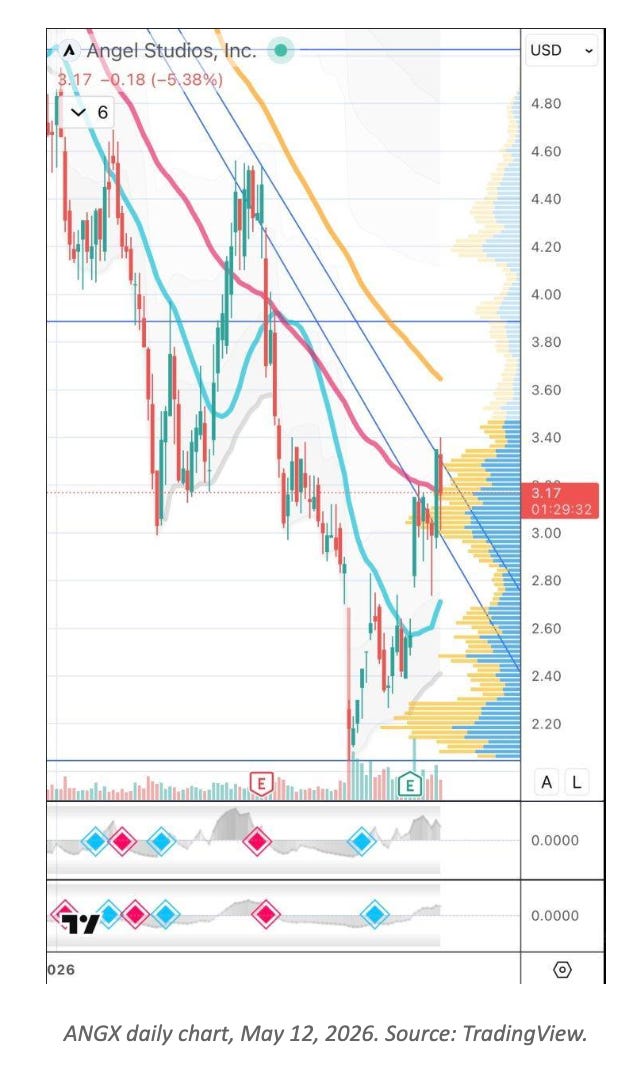

Technicals

The chart is doing something nobody is watching.

Stock got crushed from $60 down to $2.05 over nine months. A 96% drawdown empties out every weak hand on the tape. What’s left of the float belongs to people unbothered by single-digit prints. Strong hands by default, because everyone who could capitulate already did. The interesting part is what the chart looks like after that kind of move finishes draining.

Price now sits at $3.17. The 20-day moving average (cyan on the chart) just rolled over from acting as resistance into acting as support for the first time in months. That’s the first technical change worth registering. The 50-day (pink) is the next overhead test, and the 200-day (orange) sits up near $4.00. Volume on the recent leg higher came in well above the 50-day average. Earnings was the catalyst. Adjusted EBITDA flipped positive a quarter ahead of expectations on May 5, and the tape responded immediately. The green E marker on the chart is where it started.

The Bottom Line

ANGX is the only audience-curated film studio at scale running a recurring subscription engine that just turned the corner to adjusted EBITDA positive. The Guild does $365mm in ARR. The equity trades at 1.6x ARR while every relevant streaming comp trades 3x to 8x. A board director just bought a million dollars of common at $3.06. Management is acquiring three IP franchises at $6.13 per share, which is roughly 2x current price. The five-year DCF supports $16. The Rotten Tomatoes 93% audience score is hard to argue with. The cultural tailwind is real and not yet in the multiple.

The thesis breaks if churn is materially worse than implied, if the cultural tailwind reverses faster than expected, or if another dilutive raise drops below $2. None is base case.

Sub-$4 is the buy zone. Under $3 calls for size. Ten dollars is where some comes off the table. Sixteen is the target.

DISCLOSURES

This report is for informational purposes only and does not constitute investment, legal, or tax advice, nor an offer or solicitation to buy or sell any security. The information presented has been compiled from publicly available sources believed to be reliable, but accuracy and completeness are not guaranteed. Readers should conduct their own due diligence and consult qualified professionals before making any investment decision.

The author and an immediate family member hold beneficial ownership of Angel Studios, Inc. (NYSE: ANGX) securities. The author’s father participated in Southport Acquisition Corporation, the special purpose acquisition company that completed its business combination with Angel Studios in September 2025. Guardian Research has received no compensation from the Company or any related party in connection with this report.

Past performance is not indicative of future results.

Hi, Can you please add me to your discord channel ? My handle - ajinkya0726